What tax changes will affect retailers in 2024?

It might be an exaggeration to say these are the best of times and the worst of times for retailers, but positive and negative indicators for the retail industry certainly are afoot.

Let’s start with the positive.

Monthly retail sales in the U.S. are still growing, up 0.7% in September 2023 over August and up 3.8% year over year. The country’s Top 100 retailers had all grown as of July 2023, “at more or less the same rate.” And U.S. retail sales (minus automotive) were projected to rise 3.7% during the holiday season, November 1 to December 24, 2023. So that’s good.

Barclays is “bullish on retail for 2024”: The bank predicts apparel, ecommerce, and specialty retail to perform well in 2024 as inflation subsides and inventory pressures recede. InvestorPlace also expects apparel and automotive to perform well, along with specialty retail. What’s more, discount stores, dollar stores, and warehouse clubs are thriving, accounting for nearly 40% of store openings announced during the first half of 2023.

There are other reasons to be optimistic. The growing popularity of recommerce — sales of used or “pre-loved” items — is good both for the wallet and the environment. Artificial intelligence (AI) and digitalization are improving efficiency in a host of ways, from forecasting demand to communicating with customers to streamlining logistics. And though there’s been a rash of store closings, as we’ll explain, 40% of surveyed global consumers intend to increase in-person shopping due to high shipping costs.

Now for the negative.

Bankruptcies. High rents. Inflation. Wage increases. Persistent staff shortages. Retail shrink. Facing these and other challenges, retailers may open fewer stores and close more stores than usual. More than 2,800 stores could shutter in 2023 — far fewer than the 9,300 that closed in 2019, but more than 2022’s 2,603 closures. Some retailers, like national pharmacy chains, are closing more stores than other retailers.

Looking ahead, UBS analysts anticipate the closing of 50,000 retail stores by 2027 if 25% of online orders are fulfilled by a bricks-and-clicks store. If online sales grow to account for 28% to 29% of retail sales, up to 130,000 stores could close. Sobering numbers indeed (though on a bright note, surviving stores could end up doing more business).

Not as many people seem to be looking on the bright side these days. In October 2023, the IBD/TIPP Economic Optimism Index “plummeted” to 36.3 from September’s 43.2 and was well below the market forecasts of 41.6. October marked the 26th consecutive month of economic pessimism and the reading hit its lowest point since August 2011. (The IBD/TIPP Economic Optimism Index is based on a survey of 1,200 adults and is the first gauge of consumer confidence each month.)

Whatever goes down in 2024, agility, digitalization, and an omnichannel strategy will serve retailers well.

SOURCE: Trading Economics

What the numbers tell us about the retail industry

SOURCE: Retail Insight Network

SOURCE: Insider Intelligence

SOURCE: McKinsey & Company

SOURCE: Industry Dive

SOURCE: Industry Dive

Ups and downs in the supply chain

Inventory needs return to “normal”

Many businesses stockpiled inventory during the global COVID-19 supply chain crisis, if they had the space and budget to do so and could get their hands on goods; the just-in-time inventory strategy that had served them well for years made for bare shelves. With supply chains somewhat more secure, some businesses are returning to the just-in-time model, shedding inventory and trimming warehouse capacity that’s no longer needed.

For instance, The Home Depot could save $500 million in fiscal year 2024 by reverting to pre-pandemic capacity and shaving operating costs. And apparel company PVH is “targeting a 25% decrease in its inventory-to-sales ratio by the end of 2024.” CEO Stefan Larsson explained in the Q2 2023 earnings call, “Our supply chain improvements continue to accelerate and will provide us with drastically improved inventory to sales ratio over the coming years.”

It’s good to see the supply chain stabilizing, but there will likely be more taxing times ahead.

SOURCE: Industry Dive

Climate change brings new challenges for the supply chain

Drought slowed shipping traffic through the Panama Canal in 2023. Average wait times for vessels started creeping up during the summer after the maximum ship weight and number of daily crossings were reduced to conserve water. If drought conditions continue, as is likely given El Nino weather patterns, restrictions could seep into 2024.

This is troubling news for the U.S., which receives about two-thirds of Panama Canal traffic.

And drought isn’t the only worry, for climate change can impact maritime transportation in a variety of ways. Extreme weather can force vessels to take lengthy and costly detours. Rising sea levels may flood shipping terminals. Stronger and more frequent storms at sea can topple container stacks; approximately 3,000 containers were lost overboard in 2020 alone. Heat waves expand piers, soften pavement, and deform rail tracks at ports.

Consider those possibilities — and the fact that approximately 90% of goods traded internationally are shipped by sea.

SOURCE: Wärtsilä

Strikes and theft threaten to undermine supply chain stability

United Parcel Service (UPS) narrowly averted what could have been a crippling strike in July 2023. This was good news for ecommerce, as a strike would have directly affected many online retailers’ ability to fulfill orders.

According to Digital Commerce 360, 65.6% of Top 1000 sales are by retailers using UPS. In 2022, nearly $25 billion in online sales came from retailers that use UPS exclusively for fulfillment. FedEx and the U.S. Postal Service would have been hard-pressed to pick up the slack had the strike occurred.

The automobile industry hasn’t been as fortunate. A United Auto Workers (UAW) strike that began September 15, 2023, was still in full swing on October 13, when UAW President Shawn Fain vowed to make walkouts “more financially painful and less predictable for the Big Three automakers.” It took until November 20, 2023, for the last of the strikers to ratify their new contract.

Strikes have affected other industries as well, including aerospace, airlines, drugstores, healthcare providers, and entertainment. As a result, 2023 will likely go down as a banner year for strikes: There were 453,000 U.S. workers on strike at some point between January 1 and October 5, 2023, more than double 2022’s strike count of 224,000.

What 2024 will bring is anyone’s guess.

And then there’s theft, which is as much or more of a problem along the supply chain as it is in stores. There were 566 cargo theft incidents in the United States during the second quarter of 2023, a 57% year-over-year increase compared to Q2 2022. The average loss value per reported incident was $428,409, 55% higher than the value lost during the previous quarter.

The majority of cargo thefts in Q2 2023 took place near warehouses and distribution centers, as well as in unsecured parking lots, and company truck yards and premises. There was a 17% year-over-year increase in theft of full truckloads in the second quarter, and 127 more fictitious pickups, a highly specialized form of cargo theft.

Technology could help deter cargo theft. Using mobile apps to check trucks in and out and to quickly report theft can increase the likelihood of recovering stolen cargo. Hiding GPS trackers in freight trucks enables cargo to be tracked in real time. In fact, “visibility, traceability, and location intelligence” is one of the top five “digital supply chain” management trends for 2024.

Nevertheless, theft has become an enormous problem — and it’s vexing for retailers.

SOURCE: Transport Topics

Beleaguered brick-and-mortar

Retail shrink and escalating violence plague retailers

Retail shrink is the loss of inventory to causes other than a sale, anything from breakage to containers lost at sea to theft. It’s always been a thing, but theft has gained notoriety in recent years: The internet is full of videos of people running into stores, grabbing items off shelves, and legging it.

If you haven’t experienced such thievery, consider yourself fortunate.

About 50% of known crimes are not reported to the police, according to a 2023 study of organized retail crime investigators and multistore loss prevention managers. Get your head around this: “80.92% of the respondents who estimated that less than 80% of incidents are reported said it was because police will not respond, investigate, and/or arrest.”

Reported or not, the effects of crime are real. Target closed nine stores across four states on October 21, 2023, saying, “We cannot continue operating these stores because theft and organized retail crime are threatening the safety of our team and guests, and contributing to unsustainable business performance.” Citing similar safety and security concerns, Nike permanently closed a flagship store in Portland, Oregon, in 2023. Retail theft has also cut into the profits of Dick’s Sporting Goods.

Total retail shrink has been on the rise, according to an industry survey conducted by the National Retail Federation (NRF). Losses grew from $93.9 billion in 2021 to more than $112 billion in 2022, a 19.3% increase. And while the financial losses are significant, NRF Vice President for Asset Protection and Retail Operations David Johnston cited violence and safety concerns as the main priority for all retailers.

SOURCE: FreightWaves

Businesses are trying all sorts of strategies to prevent and mitigate the losses. Of the retailers surveyed by NRF, 34% increased internal payroll, 46% added more third-party security personnel, and 53% increased their technology and software solution budgets. More than half, 54%, provide employee workplace violence training.

Not wanting to fight this alone, businesses and industry advocates are calling for government assistance and policy reform. Before deciding to permanently shutter its Northeast Portland location, for instance, Nike asked the city to assign off-duty police officers to the store. Apparently it was only after the city declined to do so that Nike made the decision to leave the neighborhood for good.

California lawmakers answered the call, though not by providing additional security. On September 30, 2023, Governor Gavin Newsom signed a bill aiming to increase worker safety throughout the state by obligating employers to develop workplace violence prevention plans as part of the state’s Occupational Safety and Health Administration (OSHA) Injury and Illness Prevention Program. The new requirements take effect July 1, 2024.

Urged on by retail and trade associations, other states are going after organized retail crime. At least 11 states enacted retail crime laws in 2022 or 2023: Alabama, Florida, Illinois, Indiana, Minnesota, Nevada, New Mexico, North Carolina, Oklahoma, Oregon, and Virginia.

Congress is interested in reducing crime, both online and in stores. Had it been enacted, the Combating Organized Retail Crime Act of 2023 would have made it easier for prosecutors to bring theft cases to federal court. And the federal Integrity, Notification, and Fairness in Online Retail Marketplaces for Consumers Act (INFORM Consumers Act), which did become law, requires online marketplaces to do more to prevent sales of counterfeit, unsafe, and stolen goods.

Because remember all that stolen freight we talked about earlier? A lot of it ends up being sold via online marketplaces.

Technology may help deter retail theft

Major retailers like CVS, Lowe’s, and Walmart are using technology to help combat retail crime. Autonomous security robots, facial-recognition cameras, license-plate readers, predictive analytic software, and radio-frequency identification (RFID) tags are among the tools helping deter criminal activity, identify thieves, and track stolen goods.

Tech vendors are starting to weave AI into existing predictive technologies too. For example, AI-assisted cameras overlooking parking lots can instantly analyze images to identify suspicious activity, then activate lights and warnings to scare off potential thieves. Artificial-intelligence surveillance systems can pick people out of thousands of hours of footage.

But it’s unclear how effective such technology really is — or whether some of it should even be permitted. Cities from Boston to San Francisco don’t allow police officers to use facial recognition technology and the American Civil Liberties Union is fighting more widely to stop the use of face recognition technology, calling it “an unprecedented threat to our privacy and civil liberties.”

Expect to hear more about this issue as 2024 unfolds.

Bricks and clicks: Omnichannel is essential (and brick-and-mortar still matters)

An omnichannel strategy is pretty much essential today: “81% of consumers expect a brand’s product content experience to be similar wherever they interact with that brand,” according to a Consumer Product Content Benchmark report.

Omnichannel is not the same as multichannel. While the latter allows customers to interact with brands in more than one form, like in-store and online, omnichannel retail provides a connected experience for consumers who sometimes shop in-store, sometimes from a laptop, and more and more from their phones. Omnichannel retailers recognize customers whether they’re buying direct, from a third-party marketplace or social media site, or in a virtual world.

And increasingly, retailers are blurring the lines between channels. Colliers reports that 39% of all retailers plan to test new retail formats over the next couple of years, and the new format retailers are most interested in testing “is an omnichannel store that enables them to introduce new features and facilities, such as collection points for online orders, ordering kiosks, and drive-up/curbside facilities.”

SOURCE: Colliers

Examples of innovative retail include:

- Nike Live stores, digitally connected living retail labs where Nike tests new products and services, and shoppers are encouraged to use the Nike app

- IKEA Plan and Order points, which are a fraction of the size of standard IKEA stores and aim to prioritize convenience and simplify shopping for urban consumers

- Panera To Go, a digital-first store offering all-digital ordering and no dine-in seating

- TikTok’s pop-up shop in London, which features book, home, living, and tech products from its TikTok Shop feature

Why would retailers open new brick-and-mortar stores when 50,000 to 130,000 existing stores could close by 2027? Because “retailers that opened brick-and-mortar locations experienced an average sales increase of 37% in their respective geographic areas.”

Experimental retail is taking businesses into new worlds too. Crocs partnered with the experiential platform Obsess to offer a metaverse shopping experience for its Jibbitz charms, decorative accessories for the unique footwear. The 3D “Jibbitz Customizer” allows consumers to create their own custom Crocs in the metaverse, and ultimately purchase a physical version of their customized clog. This isn’t the brand’s first foray into virtual commerce, and Crocs certainly isn’t the only brand exploring this new frontier.

Omnichannel selling can complicate sales tax compliance

While omnichannel selling benefits consumers, it can complicate sales and use tax compliance for the retailer.

You’re more likely to trigger sales tax nexus — a connection that establishes an obligation to collect sales tax — in states where you sell through multiple avenues. It’s easier to reach a state’s economic nexus threshold when you sell through marketplaces, social media sites, and the metaverse as well as through your own website. And if you sell through a third party, inventory held in a marketplace-owned fulfillment center may create physical presence nexus.

Once registered for sales tax in a state, businesses need to keep track of changing tax rates, regulations, and rules to ensure tax is collected as required for each taxable transaction. With more than 13,000 sales and use tax jurisdictions in the United States, this is easier said than done. After all, in 2023 alone there were:

- 11,192 sales and use tax rate updates in the U.S.

- 85,836 taxability updates in the U.S. and Canada

- 98,910 sales tax holiday rule updates in the U.S

Retailers that make exempt transactions in addition to or in lieu of taxable sales face additional challenges: They need to collect a valid exemption certificate or resale certificate from the buyer, ideally at the time of sale, and keep that document up to date. The more streamlined this process, the better: It’s no fun to hound a customer for a valid certificate after a sale is complete; it’s a hassle to refund sales tax after the fact; and it would be a shame to lose the sale to a competitor that can accept a digital certificate at the point of sale.

Failure to provide a valid certificate at the time of sale can also backfire for the buyer. To wit, the District of Columbia Office of Tax and Revenue (OTR) determined that a buyer was not eligible for a refund of nearly $1 million in sales taxes paid because it didn’t provide the seller with a resale certificate at the time of the purchase, as required by D.C. Code § 47-2010. The OTR’s decision was upheld by the courts.

Reporting sales tax can also be more challenging for omnichannel retailers because it necessitates consolidating information from multiple sources. Furthermore, reporting requirements vary from state to state. Some states require retailers to report both direct and marketplace sales; in other states, retailers need only report their direct sales. You may be required to make prepayments in some states, file electronically in others, and so on.

Since trying to manually manage sales tax from disparate systems is an exercise in frustration, savvy omnichannel sellers use cloud-based sales tax software that:

- Automatically updates product taxability rules and rates, using geolocation technology to pinpoint the point of sale

- Validates and manages exemption certificates digitally

- Aggregates sales data from all sales systems

Keep in mind that retailers based outside of the U.S. can establish sales tax nexus too. The Avalara sales tax risk assessment can help you determine if and where you need to register to collect and remit sales tax, wherever your business is based.

Getting sales tax right is essential because it impacts customer experiences — and retaining customers is as critical as finding new ones.

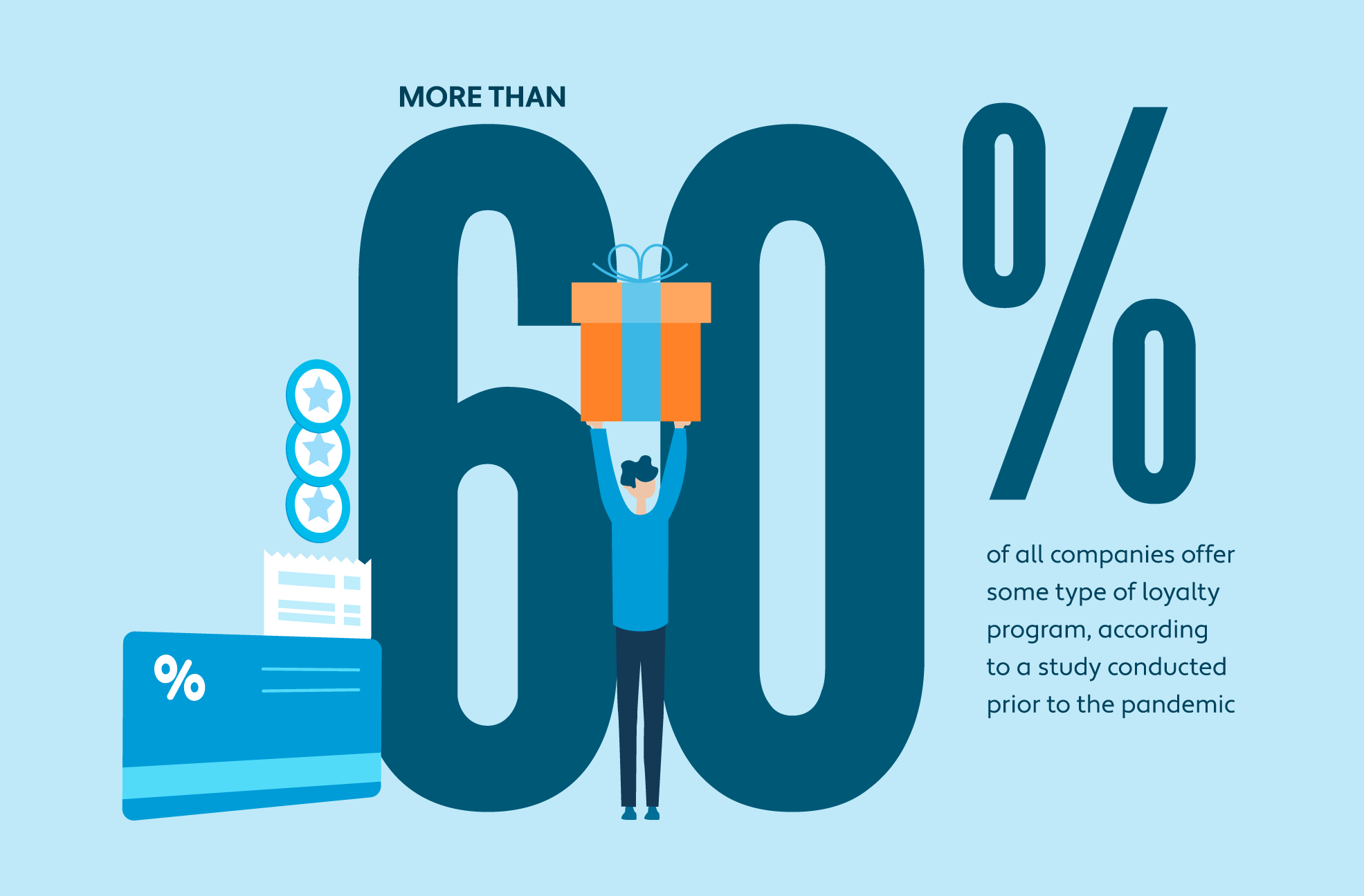

Do loyalty programs pay?

Under Armour has a loyalty program for the first time ever. Meanwhile, Amazon is making its loyalty program less exclusive by expanding grocery delivery services to non-Prime members. So, do loyalty programs work?

More than 60% of all companies offer some type of loyalty program, and the average American consumer belongs to more than 14 customer loyalty programs, according to a study conducted by Harvard Business Review prior to the pandemic. Yet another survey tells us only 42% of brand executives think their customer loyalty programs are effective.

SOURCE: HBR

After analyzing two years of purchase data from more than 10,000 customers at a top U.S. retailer, researchers determined “loyalty programs do increase profitability — but only for some customers, and not the ones you might think.” In this study, loyalty programs had little to no impact on “customers with high levels of past spending.” However, they were found to increase spending by nearly 50% for “customers who were highly vulnerable to competitors.”

The study also found loyalty programs to make a “significant difference” on two customer segments identified as consolidators and upgraders. After joining a loyalty program, consolidators started buying more products from the retailer, while upgraders bought more expensive or premium versions of products previously purchased from the retailer.

Buy now, pay later trends

Allowing customers to buy now, pay later (BNPL) can also encourage loyalty to a brand.

BNPL programs are projected to drive $17 billion in online spending during the 2023 holiday season, a $3.5 billion year-over-year increase. According to research by Adobe, one in five survey respondents planned to use BNPL to purchase gifts during the 2023 holiday season, and BNPL spend could reach $782 billion on Cyber Monday alone.

The global BNPL market was valued at $141.8 billion in 2021 and is anticipated to have a 33.3% compound annual growth rate (CAGR) through 2026. Buy now, pay later programs basically function like a point-of-sale loan, but they generally aren’t regulated as other loans are. That’s starting to change.

In October 2023, the Council of the European Union adopted a consumer credit directive designed to “protect consumers from irresponsible lending practices that spread particularly in online environments” by ensuring consumers “have all the information they need, … presented clearly, even for small-scale credit.” The directive specifically includes loans below €200 and buy-now-pay-later products.

BNPL programs are also being scrutinized in the U.S. In September 2022, the Federal Trade Commission reminded that basic consumer protection ground rules apply to anyone playing “a role in the BNPL ecosystem.” And in March 2023, the Consumer Financial Protection Bureau reported that although many borrowers use BNPL plans “without any noticeable indications of financial stress,” BNPL borrowers tended to be “much more likely to be highly indebted, revolve on their credit cards, have delinquencies in traditional credit products, and use high-interest financial services such as payday, pawn, and overdraft.”

Expect policymakers to take more interest in BNPL in 2024, and perhaps set additional regulations.

How sales tax works with buy now, pay later programs

Bear in mind that buy now, pay later programs can have sales tax implications. Retailers that offer or accept BNPL are generally responsible for determining whether and how sales tax applies to BNPL transactions. States do not take a uniform approach: Depending on the state, sales tax may be due on the full purchase at the time of the first payment, or a percentage of the tax due may be applied to each installment. Moreover, fees associated with BNPL may be subject to sales tax or they may be exempt.

Jeffrey Lutters, Director of Product Solution Engineering at Avalara, says BNPL is a new concept, so state tax law is still catching up. “Some states are grouping it with layaway rules; others are simply treating it as a straight sale, so all the tax is due up front.”

Here’s how some jurisdictions treat layaway sales: The District of Columbia requires vendors to report and remit sales tax on the entire sales amount at the beginning of the layaway, “when the sale, agreement, or other arrangement for transfer of the property from the vendor to the purchaser is made” (D.C. Mun. Regs. 409). The policy is similar in Pennsylvania, but in Arizona, tax must be collected when “title or possession transfers to the purchaser or at the time receipts from the transaction are determined to be nonrefundable, whichever occurs first” (Ariz. Admin. Code R15-5-131).

California is more like Arizona than D.C. or Pennsylvania: “There is no taxable sale until the full purchase price is paid, unless the parties agree that title will pass at an earlier date.” Same goes for Washington, though there’s no caveat for passing title to the buyer at an earlier date. In South Carolina, retailers collect sales tax incrementally; payments are “taxable in the month during which such amounts are received.”

Whether buying now or later, if a transaction occurs online, the goods will likely need to be delivered. That’s got some states looking to monetize retail delivery.

Retail delivery fee woes

Demand for urban last-mile delivery will likely grow by 78% by 2030, leading to 36% more delivery vehicles in the world’s top 100 cities. Urban deliveries could add 11 minutes to daily commute times and increase carbon emissions by 30% without effective intervention, according to the World Economic Forum. And those statistics were published in January 2020, before the spike in online sales (and therefore deliveries) caused by the pandemic.

SOURCE: World Economic Forum

All these delivery vehicles are taking a toll on the nation’s roads, and with fuel tax revenues declining as a result of improved fuel efficiency and the shift toward fully electric vehicles, new sources of revenue are needed. Enter retail delivery fees.

Colorado was the first state to implement a retail delivery fee (RDF). When it took effect on July 1, 2022, all businesses making retail deliveries of taxable goods by motor vehicle in the state were required to collect the 27-cent fee from customers and to separately state it on invoices. That proved mighty problematic because the fee’s initial requirements didn’t fit neatly into most invoicing systems, and businesses weren’t given much time to make the necessary changes.

The Colorado RDF also caused a kerfuffle for the Colorado Department of Revenue (CDOR) because CDOR was required by law to enforce the fee before it could work out many of the fee’s collection and remittance details. When the department fielded questions from taxpayers on June 23, 2022, mere days before the fee took effect on July 1, 2022, there were questions it could not answer.

Colorado ultimately eliminated some of the most challenging requirements for retailers. As of April 1, 2023, businesses are not required to separately state the fee on invoices and may pay the fee on behalf of the purchaser. Moreover, new businesses and those with $500,000 or less of retail sales in the state are exempt from the Colorado retail delivery fee (which jumped to 28 cents on July 1, 2023).

Other states and even municipalities have been watching Colorado’s RDF journey with interest, as states tend to do. Minnesota enacted a retail delivery fee in May 2023. Starting July 1, 2024, its 50-cent fee applies to retail deliveries, defined as a delivery of “1) tangible personal property that is subject to state sales tax, and 2) clothing, except for diapers.” The fee kicks in only if the pretax sale total of eligible items exceeds $100, and only once per transaction no matter how many items or shipments it takes to complete the transaction.

Taking a cue from Colorado, Minnesota provides an exception for retailers whose retail sales totaled less than $1 million in the previous calendar year, and for marketplace providers facilitating the sale of a retailer qualifying for the small seller exception. Minnesota also allows — but doesn’t require — retailers to collect the fee from purchasers. Retailers that choose to collect it must separately list the fee on a receipt or invoice. All retailers subject to the fee must remit it to the commissioner of revenue on the same filing cycle required for sales tax.

That’s not to say the Minnesota fee poses no compliance challenges. The fact that clothing is subject to the fee despite generally being exempt from Minnesota sales tax leads one to wonder whether clothing retailers will be required to obtain a Minnesota tax license. How will the fee be reported, and what will reporting look like for clothing retailers?

David Lingerfelt, Senior Director of Indirect Tax at Avalara, thinks we’ll see more retail delivery fees. “Retail delivery fees are an easy way to raise the sales tax without raising the sales tax.” And indeed, at least two online delivery fees were introduced in New York during the 2023 legislative session (one for the state and one for New York City), and Washington is studying the possibility of a retail delivery fee.

Retail delivery fees appeal to policymakers for several reasons: They could help reduce traffic congestion and reduce emissions from heavy delivery traffic. And of course they bring in revenue: Colorado estimates that its RDF will generate $18.8 million in revenue in its first two years, while Minnesota’s fee could bring in $46.4 million in its first year alone.

That doesn’t bode well for retailers. Businesses subject to such fees need to figure out whether and how to charge customers the fee. They also need to ensure their sales systems can capture any and all RDFs where applicable, based on the rules and rates set by each jurisdiction, and that they properly report both the fees and any sales taxes due on the fees. Avalara can help customers on both sides of the transaction.

Going green

Consumers may not like paying retail delivery fees, but some may be willing to pay a bit more for greener products.

According to the EY Future Consumer Index, 24% of GenZ and Millennials check brands’ sustainability claims and 21% will stop buying a product if the brand isn’t “making enough effort to help the environment.” In another study, 75% of Millennials were found to be “eco-conscious to the point of changing their buying habits to favor environmentally friendly products.”

That said, some consumers aren’t willing to sacrifice their wallets for their ideals.

SOURCE: White & Case

Key environmental, sustainability, and governance (ESG) issues for the retail industry include decarbonization, green contracts, greenwashing, supply chains, and the circular economy — the growing trend to reuse or resell products instead of discarding them. This is known as recommerce.

Recommerce

Revenue from global recommerce is on track to nearly double by 2027, reaching $350 billion, according to the thredUP Resale Report. It’s also on track to grow three times faster than traditional retail through 2030.

This isn’t a new phenomenon: In a 2022 eBay report on recommerce, 90% of buyers surveyed said they’d purchased pre-loved goods on eBay in the past year, and 90% of eBay sellers surveyed said reducing waste was an important aspect of recommerce. “In 2022, eBay recommerce resulted in 73,000 metric tons of waste avoided from landfills, 1.6 million metric tons of avoided carbon, and $4.6 billion in positive economic impact created by eBay’s sellers and buyers.”

Retailers that enter the recommerce space should pay close attention to the potential tax consequences. If you create a resale site, you may turn yourself into a marketplace facilitator and could end up liable for collecting and remitting the tax due on sales made through the site. When you consider that there were more than a million active users participating in just one fashion brand’s resale ecosystem as of March 2023, it becomes clear how quickly tax liability can add up.

The tax implications of merchandise returns

Keeping used products out of landfills is one good reason to encourage recommerce. Another is the high cost of processing returns. Of the retailers surveyed by Pollfish, 73% rank returns as a “moderate-to-severe issue for their business.” Another survey found that online returns cost retailers an average of 21% of order value, and that 70% of retailers are “actively trying to lower the cost of returns.”

These are sobering statistics, especially when you consider that returned merchandise jumped from 10.6% of total retail sales in 2020 to 16.6% in 2021 and 16.5% in 2022.

SOURCE: Practical Ecommerce

Returns can be a hassle for sales tax compliance. Both customers and tax authorities will check to see that sales tax was refunded or credited as permitted by law. Since sales tax policies related to returns vary by state, as sales tax policies generally do, this can be hard on retailers doing business in multiple states.

Consumers in Connecticut aren’t entitled to a refund of sales tax (at the rate paid on the original sale) if the return occurs more than 90 days after the original purchase date, and that’s not uncommon. If the return takes place within the 90-day window, the amount of sales tax due depends on the amount of the refund. For instance, a consumer who paid $6.35 in sales tax on a $100 bicycle would only be refunded $5.72 if the retailer takes a $10 restocking fee out of the $100 sales price and therefore refunds the consumer $90 instead of the full $100 they initially paid.

That’s just one scenario; there are many others. If you’re responsible for collecting and remitting sales tax in multiple states, you need to understand and comply with the requirements in each of those states. Automating the collection and remittance of sales tax can help.

Bag fees

Also implemented for environmental reasons, bag fees can be another bugbear for retailers.

Most bag fees are local, and they aren’t new. Examples include the 10-cent fee on plastic and paper bags in Batavia, Illinois, the 15-cent fee for paper shopping bags and $1 fee (minimum) for new reusable bags in Edmonton, Alberta, Canada, and the 5-cent tax on each disposable plastic bag provided to customers in some cities and counties in Virginia. Local bag fees are generally administered by the local taxing authority, but Virginia's disposable plastic bag tax is collected, administered, and enforced by the Virginia Tax Commissioner.

While local bag fees will undoubtedly proliferate, Colorado and Washington could start a new trend with statewide bag fees.

The Colorado bag fee

Between January 1, 2023, and January 1, 2024, stores in Colorado may give customers a recycled paper or single-use plastic carryout bag at the point of sale if and only if the customer pays a fee for the bag. The fee is 10 cents per bag unless there’s a higher local fee in the county or municipality where the store is located. Certain exceptions apply.

Once collected, the bag fee must be tucked away for good keeping. Stores are required to remit 60% of the carryout bag fee to the municipality or county in which the store is located, on a quarterly basis, starting April 1, 2024. That’s unusual, to say the least. Retailers may retain the remaining 40%.

Also unusual: Although it’s a state fee, retailers don’t remit any portion of the fee to the Colorado Department of Revenue.

The bag fee isn’t subject to Colorado state sales tax or state-administered local sales taxes. However, it may be subject to local sales tax in self-collecting home-rule municipalities. Retailers are encouraged to contact local finance departments for additional information.

For the most part, single-use plastic carryout bags will be banned in Colorado as of January 1, 2024, but the fee will continue to apply to paper bags.

The Washington bag fee

Washington state currently requires retail establishments to collect an 8-cent fee for every compliant paper bag or reusable film-plastic carryout bag they provide or sell. Starting January 1, 2026, the 8-cent charge will jump to 12 cents per bag for reusable carryout bags made of plastic films, but will remain 8 cents per compliant paper bag. Any local bag fees in Washington state that were enacted prior to April 1, 2020, and are still in effect will be replaced by a statewide bag fee beginning January 1, 2026.

Though retained by the retailer, the Washington fee must be separately stated and reported as a retail sale. Washington sales tax applies to the state bag fee even if the goods being purchased, like food for home consumption, are exempt. Bag fees are considered a retail sale and must be reported under the Retailing Business and Occupation (B&O) tax classification and under the retail sales tax classification. However, the retailer can take a deduction for the compliant carryout bag charge, so retailers don’t have to pay B&O tax on the charge. The bag charge is retained by the retailer, not remitted to the departments of revenue or ecology.

Retailers subject to bag fees in different parts of the country must be sure to collect, report, and tax them as required. Like the retail delivery fees discussed earlier, these fees can become yet another compliance burden for affected businesses.

“Bag fees and the retail delivery fees were created for entirely different reasons,” notes Scott Peterson, VP of Government Relations at Avalara, “but complexity is what they have in common.”

Now, let’s move on to the fun stuff, like sales tax trends.

Taxability trends

Sales tax exemptions are in vogue, new sales taxes are out — except where they’re not.

Sales tax exemptions sweep the country

Most states started 2022 with pockets full of cash, and with pockets still jingling at the end of the year, most expected revenue to continue to grow through 2023. The governor of Rhode Island kicked off 2023 with a proposal to reduce the state sales tax while his colleague in South Dakota sought to eliminate the sales tax on groceries, as did the governor of Kansas. Several other states, including Arizona and Kansas, sought to exempt diapers and/or feminine hygiene products.

So, what happened?

Several states reduced or eliminated taxes on food

The Illinois 1% sales tax on groceries was suspended from July 1, 2022, through June 30, 2023. And food for home consumption and essential personal hygiene items became exempt from state sales and use tax in Virginia as of January 1, 2023, though the 1% local option tax still applies.

Kansas cut the state sales tax on food, food ingredients, and certain prepared food from 6.5% to 4% effective January 1, 2023; the state sales tax rate on food drops to 2% on January 1, 2024, and will hit 0% starting January 1, 2025.

There’s more. The Alabama state sales tax on food dropped from 4% to 3% on September 1, 2023. It will decrease from 3% to 2% effective September 1, 2024, provided there’s “sufficient growth in the state Education Trust Fund.” City and county sales tax rates will be equal to their general sales tax rate in effect as of June 15, 2023, though local governments can lower the tax rate on food in 25% increments any year in which there’s sufficient growth in their local general fund.

Instead of reducing the tax on groceries, as the governor wanted, South Dakota reduced the state sales tax rate from 4.5% to 4.2% starting July 1, 2023. The Mount Rushmore State could further reduce or even eliminate the state sales tax rate on groceries if the issue makes the November 2024 ballot in the form of an initiated constitutional amendment and an initiated measure. We’ll have to wait and see.

Food isn’t the only product benefitting from exemptions.

Two more states exempt separately stated delivery charges

Most delivery charges and installation charges are exempt from Michigan sales tax as of April 26, 2023, as long as the seller separately states the charges on the customer invoice and keeps books and records showing how tax was levied and calculated for these transactions. Likewise, separately stated delivery charges are exempt from Kansas sales tax effective July 1, 2023.

Don’t be surprised if there are more taxability changes related to delivery services in 2024.

There are new exemptions for family (especially women’s) health products

North Carolina’s new budget, which became law without the governor’s signature on October 3, 2023, establishes a sales and use tax exemption for breast pumps, breast pump collection and storage supplies, and repair and replacement parts. Bottles, nursing bras, and other related products remain taxable unless part of a qualifying, prepackaged breast pump kit. The exemption took effect November 1, 2023.

A sales and use tax exemption for baby and toddler products took effect in Florida on July 1, 2023. Qualifying products include baby and toddler clothing, changing tables, diapers, playpens, and safety gates, as well as breast pumps and related products. A few months later, on October 1, 2023, diapers for children, car seats, and several other children’s products became tax free in Ohio.

The state sales tax ceased to apply to essential personal hygiene products in Virginia as of January 1, 2023, though the 1% local option sales tax still applies to these sales. And as of September 1, 2023, Texas no longer taxes certain family care items: baby bottles and wipes, breast milk pumping products, feminine hygiene products, maternity clothing, and wound care dressings.

We expect to see more so-called pink tax exemptions in 2024. Advocacy groups in Arkansas have put forward a ballot initiative to exempt feminine hygiene products and diapers from state sales tax. (Arkansas is one of about 20 states where period products are subject to tax.) And the Streamlined Sales Tax Governing Board (SSTGB, or simply SST) is looking to clarify definitions related to menstrual products and to specify whether newer products like period underwear and menstrual cups should be exempt.

Sales tax exemptions promote gun safety

Certain firearm safety devices are exempt from Florida sales and use tax as of July 1, 2023, and Tennessee exempts firearm safes and firearm safety devices from sales and use tax starting November 1, 2023. The Volunteer State test-drove the exemption with a lengthy sales tax holiday for gun safes and safety devices, which lasted from July 1, 2021, through June 30, 2023.

Michigan adopted a sales tax exemption for firearm safety devices in 2023 with the enactment of Senate Bills 81 and 82, but the exemption will sunset December 31, 2024. Sales tax exemptions for gun safes and/or safety devices were also proposed in more than a half dozen other states, including Alabama, California, North Carolina, Ohio, Oklahoma, Rhode Island, and Wisconsin.

Miscellaneous sales tax exemptions

It’s common for states to exempt certain products or services just because they can. (OK, not really, but it would take too long to dive into each and every origin story.) For 2023, these one-offs include:

- A Florida sales and use tax exemption for services provided by certain small private investigative agencies (effective July 1, 2023)

- A Kentucky exemption for marketing services (effective retroactively to January 1, 2023)

- A New Mexico gross receipts tax exemption for ebook licenses purchased by public libraries (effective July 1, 2023)

- An Ohio exemption for the consumer-grade fireworks fee (effective October 1, 2023)

- A Texas exemption for the service of furnishing an academic transcript (effective October 1, 2023)

2024 will almost certainly bring another slew of sales tax exemptions.

New sales taxes take a stand

Of course, it’s not all about sales tax exemptions. Numerous states are broadening sales tax to previously untaxed goods and services.

California will apply an 11% tax to gross receipts from retail sales of ammunition, firearms, and firearm precursor parts starting July 1, 2024. New York and Wisconsin are also interested in imposing a tax on firearms manufacturers for each firearm made that’s offered for sale in the state.

SOURCES: Avalara, Wisconsin Legislature, Avalara

North Carolina established a new tax on for-hire ground transport services. The transportation commerce tax will apply to exclusive and shared for-hire ground transport services starting July 1, 2025.

Texas didn’t create a new tax on fireworks, but it now allows fireworks to be sold for Diwali: Firework sales, which are subject to Texas sales tax, are now permitted beginning five days before the first day of Diwali and ending at midnight on the last day of Diwali.

Kentucky clarified how tax applies to certain services that were made taxable by a law enacted in 2022. We now know that as of January 1, 2023, extended warranty services (including prewritten computer software access services) are subject to sales tax. And tax applies only to limited testing processes performed in a laboratory, rather than general testing services. Kentucky also updated sourcing guidelines for retail sales of services subject to Kentucky sales and use tax.

There’s a good chance some states will pass laws related to ticket sales and fees in 2024 (largely thanks to the ticketing bots that snatched up Taylor Swift concert tickets at the speed of light then resold them at extortion prices). According to a podcast by the National Conference of State Legislatures, “the snafu became the catalyst for 24 states and Puerto Rico to consider 70 bills addressing ticket sales and fees.” Some of those could involve sales tax.

Practically every day is a (sales tax) holiday … in Florida

The past couple of years have seen a lot of activity centered on sales tax holidays. Remember that impressive stat from earlier? There were 98,910 U.S. sales tax holiday rule updates in 2023.

David Lingerfelt expects we’ll see more sales tax holidays, longer sales tax holidays, and broader sales tax holidays in 2024. Consumers love them after all. “Sales tax holidays are becoming less about tax policy and more about politics,” Lingerfelt says. “They make a political statement and have tax implications.” He finds this to be particularly true in Florida and Texas, and he predicts we’ll see more in other states in the coming years.

Florida’s sales tax holidays are legendary in the sales tax community, and with good reason. The state has taken to offering six or seven overlapping sales tax holidays per year, putting retailers in a pickle.

For instance, would a flashlight sold on September 3, 2023, qualify for Florida’s Freedom Summer sales tax holiday, the disaster preparedness sales tax holiday, or the tool time sales tax holiday? It matters, because flashlights eligible for the exemption are subject to a $30 price cap under the first, a $40 price cap under the second, and a $50 price cap under the third. Plus, each sales tax holiday starts and ends on a different date.

SOURCE: Florida Department of Revenue

What’s a retailer to do?

Florida and other states also seem to be testing how far they can stretch a sales tax holiday before it breaks. Historically, these temporary exemptions last a day, a weekend, or perhaps a week. But months? A year? Two years? Is a sales tax holiday really just a vacation from sales tax if it lasts that long? (Try taking a year or two off work and see what happens.)

A Streamlined Sales Tax advisory council is studying sales tax holidays. Among other issues, it’s seeking answers to such questions as: “What is [a] ‘sales tax holiday’ versus a ‘regular sales tax exemption with a sunset?’” and “Is there a maximum amount of time an exemption needs to be in place for it not to be a sales tax holiday?” It will be interesting to learn what the council decides.

For now, at any rate, sales tax holidays are hard on retailers in general, and online sellers and marketplaces in particular. According to the National Conference of State Legislatures, sales tax holidays are a burden for some businesses: “The administrative work required to exempt eligible products from sales tax can be time-consuming and difficult because the list tends to be very specific and limited to a dollar amount. Additionally, businesses must ensure that local taxes are applied when local governments opt out of state sales tax holidays.”

A sales tax holiday can also be a “gotcha” moment for businesses not registered to collect and remit sales in the state. If sales increase markedly during a sales tax holiday, as they’re wont to do, that can catapult a retailer over an economic nexus threshold and into sales tax liability land.

Per the Retailers Association of Massachusetts, the Bay State’s annual sales tax holiday generates about half a billion dollars each year for Massachusetts businesses. Given that figure, the tax-free weekend could certainly lead to new sales tax obligations for out-of-state online sellers — including marketplace facilitators.

Online sales tax: Marketplace makeover

Ecommerce sales in the United States are predicted to grow by $588 billion over the next five years, and marketplaces should account for roughly 40% of those gains. Some of the growth will come from established brands and retailers opening their own third-party marketplaces. This rapid gain of market share is one reason states are refining their marketplace facilitator laws.

SOURCE: Insider Intelligence

All states with a general sales tax, plus Puerto Rico, Washington, D.C., and numerous local jurisdictions in Alaska, have marketplace facilitator laws requiring marketplace facilitators to collect and remit the sales tax due on all sales made through the platform. These marketplace facilitator laws were supposed to not only increase sales tax collections for states, but to simplify sales tax compliance for third-party sellers (if not for the marketplaces).

Have marketplace facilitator laws actually simplified compliance for businesses? Not so much.

In a survey of 1,000 U.S. and U.K. businesses conducted shortly before the fifth anniversary of the U.S. Supreme Court decision in South Dakota v. Wayfair, Inc., 41.2% of respondents reported an increase in overall complexity of managing tax requirements as a result of marketplace facilitator laws. Furthermore:

- 34.6% of respondents said marketplace facilitator laws have increased compliance costs

- 37.9% said marketplace facilitator laws have increased the time required to manage tax requirements

- 33.5% said marketplace facilitator laws have increased the number of states/regions they now have to register, collect, and file taxes

SOURCE: Avalara

One reason for the complexity: Many states are grappling with what is, and what isn’t, a marketplace for sales tax purposes. They’re also continually tweaking the taxes marketplaces are required to collect and remit. The complexity will likely grow as marketplaces make like Captain Kirk and boldly go where no marketplace has gone before (i.e., to virtual worlds).

What is, and what isn’t, a marketplace?

There are all sorts of marketplaces in businesses today. If you’re moving, you can find strong backs on a marketplace like Craigslist or Thumbtack. Want help cleaning your gutters, painting a room, or putting together IKEA furniture? Check out a marketplace like Taskrabbit. Should you have an insatiable appetite for toys, marketplaces like eBay and Etsy, as well as niche platforms like FiddlePiddle, have you covered.

For the most part, marketplace facilitator laws are clear when it comes to a marketplace that sells new or used taxable tangible personal property. The waters get muddier in other situations, such as when a marketplace deals in beverage alcohol, food delivery, lodging, or rideshares, or when a platform connects buyers and sellers but doesn’t process payments. If any of these situations apply to you, keep in mind that while you may not be subject to sales tax in State X or Y today, you could be tomorrow.

Moreover, states are continually modifying their marketplace facilitator laws.

In August 2023, the California Department of Tax and Fee Administration (CDTFA) issued a long-awaited final regulation governing the taxability of marketplace transactions. In a nutshell, any business handling the fulfillment, payment, or storage of products for sale is a marketplace facilitator responsible for California sales tax, as is any business listing products, setting prices, providing customer service, or taking orders on behalf of a marketplace seller.

That’s not all. The CDTFA considers you to be a marketplace facilitator if you accept orders and transmit offers between a buyer and a seller, operate a marketplace website, or provide virtual currency to buyers so they can pay sellers. On the other hand, if you merely refer a buyer to a seller (via a link, ad, or direct referral), you’re not a marketplace facilitator in the eyes of California.

And if you’re a delivery network company, meaning you maintain an internet website or mobile application to facilitate delivery services for the sale of local products, you may elect to be treated as a marketplace facilitator — or not.

What taxes and fees are marketplace facilitators responsible for?

Well, it depends.

Louisiana eliminated the 200-or-more transaction threshold for economic nexus starting August 1, 2023. As of the same date, it limited the $100,000 sales threshold to remote retail sales instead of “all retail sales,” and limited the time frame for notification of an approval or denial of a marketplace facilitator application to not later than 30 business days after receipt of the completed application.

The Pelican State also clarified, in an information bulletin published September 8, 2023, by the Louisiana Sales and Use Tax Commission for Remote Sellers, that marketplace facilitators are required to maintain documents such as exemption certificates and taxability information.

Furthermore, marketplace facilitators are responsible for the tax due on all transactions facilitated in the state even if the third-party seller has a physical presence in Louisiana. This is true whether the marketplace facilitator itself has a physical presence in or outside of Louisiana. According to the bulletin, “Sales occurring on a marketplace that are facilitated by a marketplace facilitator are remote sales, requiring sales tax to be remitted to the Commission.”

A third-party seller with a physical presence in Louisiana, however, is responsible for any tax due on their direct (i.e., non-marketplace) sales in the state.

Other jurisdictions have also clarified that online marketplaces are responsible for collecting and remitting this or that tax. For example, as of January 1, 2023, marketplace facilitators must collect and remit other taxes administered by the state of Oklahoma, including lodging taxes. Marketplace facilitators in British Columbia are responsible for collecting and remitting Provincial Sales Tax (PST) on certain online marketplace services. And back in California, marketplace facilitators are generally required to collect and remit the California battery fee (CBF), electronic waste recycling fee, lumber products assessment (LPA), and tire fee.

SOURCE: CDTFA

Marketplace inventory update

A factor retailers should think about when considering selling through a marketplace is what happens with the inventory. Should a third-party seller be liable for sales tax in a state if the seller’s only connection, or nexus, is the presence of inventory in a marketplace fulfillment center in the state? Ask California, Washington, Wisconsin, and some other states, and the answer will almost certainly be, “yes.”

California courts have effectively authorized the CDTFA to hold unregistered out-of-state sellers liable for sales tax based on inventory held in a warehouse in the state, even when the seller didn’t realize a third-party was storing its inventory in California.

And California is just one of roughly 20 states where holding inventory in the state, including in a third-party fulfillment center or warehouse, can establish a sales tax obligation for a third-party seller. Others include the SST member states of Georgia, Rhode Island, and Vermont.

SOURCE: Avalara

Marketplace sellers have challenged this stance, and they’ve found success in at least one state. In September 2022, the Commonwealth Court of Pennsylvania held that an out-of-state business whose only connection to Pennsylvania is inventory stored in an Amazon warehouse in the state does not have nexus for Pennsylvania sales and use tax or personal income tax. The Pennsylvania Department of Revenue did not appeal the decision.

With the decision in Online Merchants Guild v. Hassel, No. 179 M.D. 2021, the Commonwealth Court of Pennsylvania became the first court to rule against a state in an inventory nexus case. There will likely be more legal battles ahead. After a California court dismissed the Online Merchants Guild (OMG) suit against California inventory nexus then refused to rehear the case, the OMG petitioned the U.S. Supreme Court to take up the case. It’s still waiting for a response.

Marketplaces as protectors of the people

Marketplace facilitators aren’t merely responsible for tax compliance. New consumer protection mandates established under the federal INFORM Consumers Act require marketplaces to do more to prevent online shopping fraud and protect consumers from counterfeit, stolen, and unsafe goods. It took effect June 27, 2023.

“Counterfeit and stolen products have become pervasive on major online marketplaces,” according to a Congressional report on the INFORM Consumers Act. Under the new law, an online marketplace must:

- Collect and verify certain information from high-volume third-party marketplace retailers

- Provide additional information for some high-volume sellers

- Provide “clear and conspicuous” reporting options for customers

- Comply with data privacy and security requirements

Under the INFORM Consumers Act, “high-volume sellers” are those with at least 200 discrete sales or transactions and an aggregate total of $5,000 or more in gross revenues during any 12-month period in the previous 24 months.

New 1099-K reporting requirements are coming … eventually

Both marketplace facilitators and marketplace sellers must also start to prepare for several new 1099-K reporting requirements on the horizon. A Form 1099-K is a report of payments received during the year from one of two types of reportable payment transactions:

- Payment card transactions (credit, debit, or stored value cards such as a gift card), or

- Third-party network transactions (payment apps or online marketplaces, including third-party payment settlement organizations)

Currently, online marketplaces, payment apps, and payment card companies are required to file a Form 1099-K with the IRS and provide a copy to any payee (e.g., marketplace seller) that receives over $20,000 in more than 200 transactions in a calendar year. The $20,000/200-transaction threshold was scheduled to drop considerably — to more than $600 with no transaction threshold — for tax years starting 2023. However, on November 21, 2023, the IRS announced a delay of the new $600 Form 1099-K reporting threshold for third-party settlement organizations.

SOURCE: IRS

This is the second time the $600 threshold has been pushed back; it was originally set to take effect for tax year 2022.

The IRS now says it will phase in the changes. For tax year 2023, 1099-K reporting will be required only if the taxpayer receives over $20,000 in more than 200 transactions in 2023. That threshold will likely drop to $5,000 for tax year 2024, and to $600 in a subsequent year. The IRS is also looking to update the Form 1040 and related schedules for 2024 to “make the reporting process easier for taxpayers.”

Whether $20,000, $5,000, or $600, the threshold includes payments for personal items sold, goods sold, services provided, or property rented through any:

- Peer-to-peer payment platform or digital wallet

- Online marketplace (sale or resale of clothing, furniture, and other items)

- Craft or maker marketplace

- Auction site

- Car-sharing or ride-hailing platform

- Real estate marketplace

- Ticket exchange or resale site

- Crowdfunding platform

- Freelance marketplace

Gifts or reimbursement of personal expenses from friends and family should not be reported on a Form 1099-K, as they are not payments for goods or services. The IRS recommends these types of payments be noted as non-business in the payment apps, when possible.

Once the 1099-K threshold is lowered, it will affect many small marketplace sellers that never reached the higher threshold of 200 transactions and $20,000 in aggregate sales. It will also affect individuals who receive $5,000 and eventually $600 or more in payments for personal items that are considered “payments for goods and services” and sold through a payment app (e.g., PayPal, Square, Venmo) or online marketplace.

Other changes affecting 1099s

The threshold for electronic filing of 1099s and other forms is being reduced from 250 returns down to 10 or more returns in a calendar year, beginning in 2024 for tax year 2023. The threshold applies to a taxpayer’s combined number of returns. As a result, many small businesses that previously filed paper returns will be required to file electronically.

For example, if you hired 15 independent contractors over the course of the year and paid each one more than $600, you’d need to electronically file 15 1099-NEC forms. If you have five employees and hired five contractors, paying each one more than $600, you’d need to electronically file five W-2s and five 1099-NEC forms. However, if you have only two employees and hired no independent contractors, you could file the five W-2s on paper.

Per the IRS, “To determine if you meet the 10 or more threshold to electronically file:

- Identify how many information returns of any type covered by TD 9972, you need to file during a calendar year

- If 10 or more, you MUST file electronically”

What else could affect the retail industry in 2024?

We’ll likely see retailers use technology like AI to streamline operations in a variety of ways, including to:

- Anticipate demand

- Assess the success of marketing and promotional activities

- Consolidate data from multiple sources

- Identify experience retail trends (like those that erupted around the “Barbie” movie and Taylor Swift’s Eras tour)

- Forecast the supply chain

- Reduce operational costs

- Respond to customer questions and concerns

- Automate markdowns and clearance processes

- Provide personalized product recommendations

SOURCE: Visionet Systems

Technology can help retailers determine the taxability of the products and services they sell as well. In fact, automation tools and AI are helping state tax departments streamline processes and disseminate tax information to businesses.

For example, Colorado and Missouri are leveraging AI-driven Avalara Tax Research to power their publicly available sales and use tax information, so retailers and other businesses can find data they need. The technology facilitates communication between state regulators and enables the states to easily keep track of ordinances, rules, taxability information, and proposed tax changes within their local jurisdictions.

“Using artificial intelligence, automation, and a team of tax experts, Avalara’s solutions and database for tax compliance rates and rules help increase the accuracy and timely validation of tax data for businesses and governments alike,” explains Jayme Fishman, EVP and GM of Indirect Tax at Avalara.

It’s very difficult to meet the demands of sales tax compliance without relying on automation and other technology. There are too many nuances and too frequent changes to rates, rules, and regulations. What you’re reading in this report gives a good idea of what’s out there, but it certainly doesn’t cover all tax changes. No one report could.

How Avalara can help

Avalara can help you account for tax changes and improve tax compliance for your business. Learn more about our automated solutions for calculating tax rates, preparing returns, and managing documents.