What sales tax changes are happening in 2024?

Income tax is out. Retail sales tax is in.

That’s just one of the trends likely to affect sales tax in 2024.

State budgets will grow increasingly dependent on sales tax revenue in 2024 and beyond, as almost 30 states have lowered corporate or personal income tax rates since the start of 2021. But “states wishing to transition from income toward consumption taxation will eventually need to reckon with long-standing issues facing the sustainability of state sales taxes,” according to the National Conference of State Legislatures.

Though sales tax is the second-largest source of state tax revenue, evolving consumer and technology trends are eroding the sales tax base. Many sales tax laws are woefully outdated.

For instance, most states don’t tax the majority of services even though services now account for approximately 70% of all personal consumption. Per the National Conference of State Legislatures, Hawaii, New Mexico, and South Dakota are the only states where a significant majority of 176 specified services are subject to sales tax.

Moreover, despite the rise of digital goods and streamed content, and the corresponding demise of the CD, DVD, and floppy disk, about half of all states still don’t tax digital products or streaming services.

This is a byproduct of changing technology. States haven’t changed what they tax; they still tax what’s sold on a CD, DVD, or floppy disk. What’s changed is that very little is delivered by CD, DVD, or floppy disk today.

“The taxation of streaming services has long been complicated by advancements in technology as well,” says Scott Peterson, VP of Government Relations at Avalara. “Long ago, cable television began to compete against broadcast television. TV watchers didn’t pay to receive broadcast television so there wasn’t anything to tax. Cable television was different because there was a charge. It didn’t take governments long to start taxing cable television.”

Many states are further weakening their sales tax base by establishing new sales tax exemptions — either permanent or temporary — for a range of consumer goods. Yet most states continue to tax many business inputs (which economists argue should be exempt).

Should certain taxable transactions be exempt? Should sales tax apply to currently exempt transactions? Are there any new and creative ways to obtain more tax revenue from retail sales? As 2024 unfolds, expect states to grapple with these questions — and more.

What the numbers tell us about sales tax in 2024

SOURCE: CBO

SOURCE: CBO

SOURCE: Tax Policy Center

SOURCE: The Conference Board

SOURCE: Resume Builder

Economic uncertainty hasn’t settled

To put the state of sales tax into perspective, it helps to start with a broader view of economic trends.

Economists predict persistent inflation, fragile growth

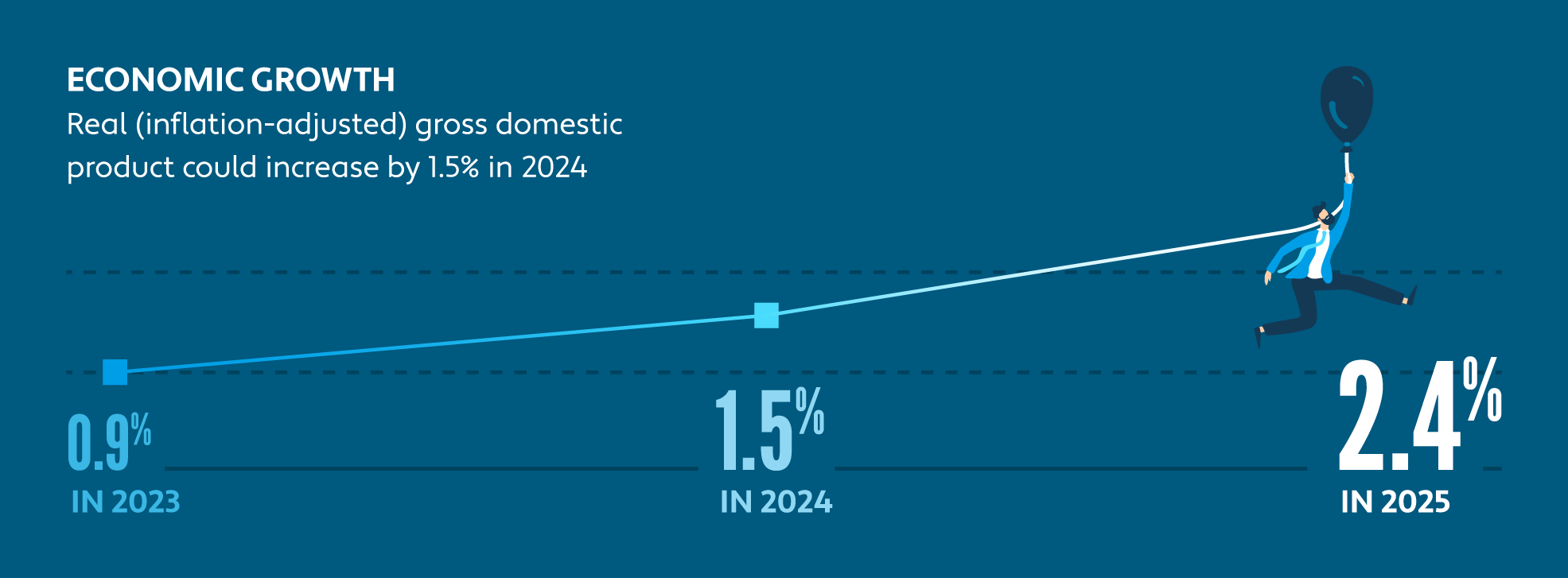

The International Monetary Fund (IMF) expects global growth to hold steady at 3% in both 2023 and 2024. That’s slightly more optimistic than the Organisation for Economic Co-operation and Development (OECD), which projects 2023’s 3% global growth rate to slow to 2.7% in 2024.

The OECD take on the American economy is more dismal still: It predicts U.S. gross domestic product (GDP) growth to slow from 2.2% in 2023 to 1.3% in 2024. More upbeat, the Congressional Budget Office (CBO) is forecasting sustained economic growth for 2023 to 2025 — though it expects “a soft patch in the near term.”

2024 state budgets are “ready and waiting for a slower economy”

About half of all states expect state tax revenues to slow in fiscal year 2024. Analysis of monthly tax collection reports shows at least 17 states experienced year-over-year declines for the 12 months ending June 30, 2023.

Fortunately, state rainy day funds reached an all-time high of $164 billion in fiscal year 2022. This “revenue cushion” should help states withstand a recession, should one come, even given increased spending on education, health care, and other needs. Indeed, Fitch Ratings reports “U.S. state budgets are ready and waiting for a slower economy in the coming months.” And, according to Bloomberg Tax Research, sales tax revenue for August increased 1% year over year in 28 states, to $29.9 billion.

Notably, taxable sales and purchases for April, May, and June of 2023 were up 16.8% in North Dakota; sales tax revenue in New York City grew 5.2% year over year during the fourth quarter of the fiscal year (April 2023 to June 2023). The positive trend extended to Texas, where Comptroller Glenn Hegar sent cities, counties, transit systems, and special purpose districts $1.1 billion in local sales tax allocations for October 2023, 4.5% more than in October 2022.

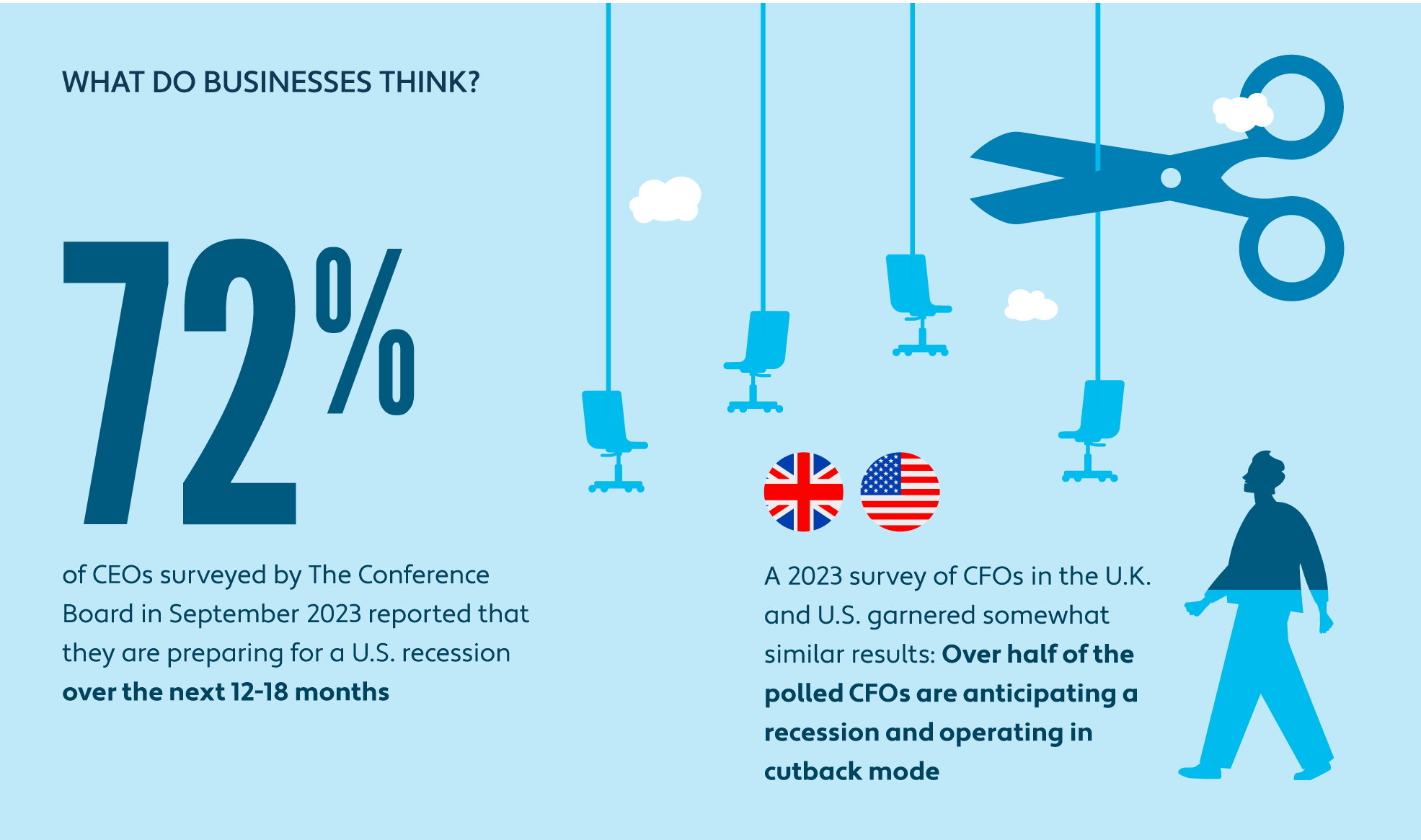

Businesses are preparing for recession

What do businesses think? Well, 72% of CEOs surveyed by The Conference Board in late September 2023 reported that they are preparing for a U.S. recession over the next 12–18 months. Of those, 69% expect “a brief and shallow recession.” An August 2023 survey of CFOs in the U.K. and U.S. garnered somewhat similar results: Over half of the polled CFOs are anticipating a recession and operating in cutback mode (using consumer spending, Consumer Price Index, and Producer Price Index as indicators of a recession).

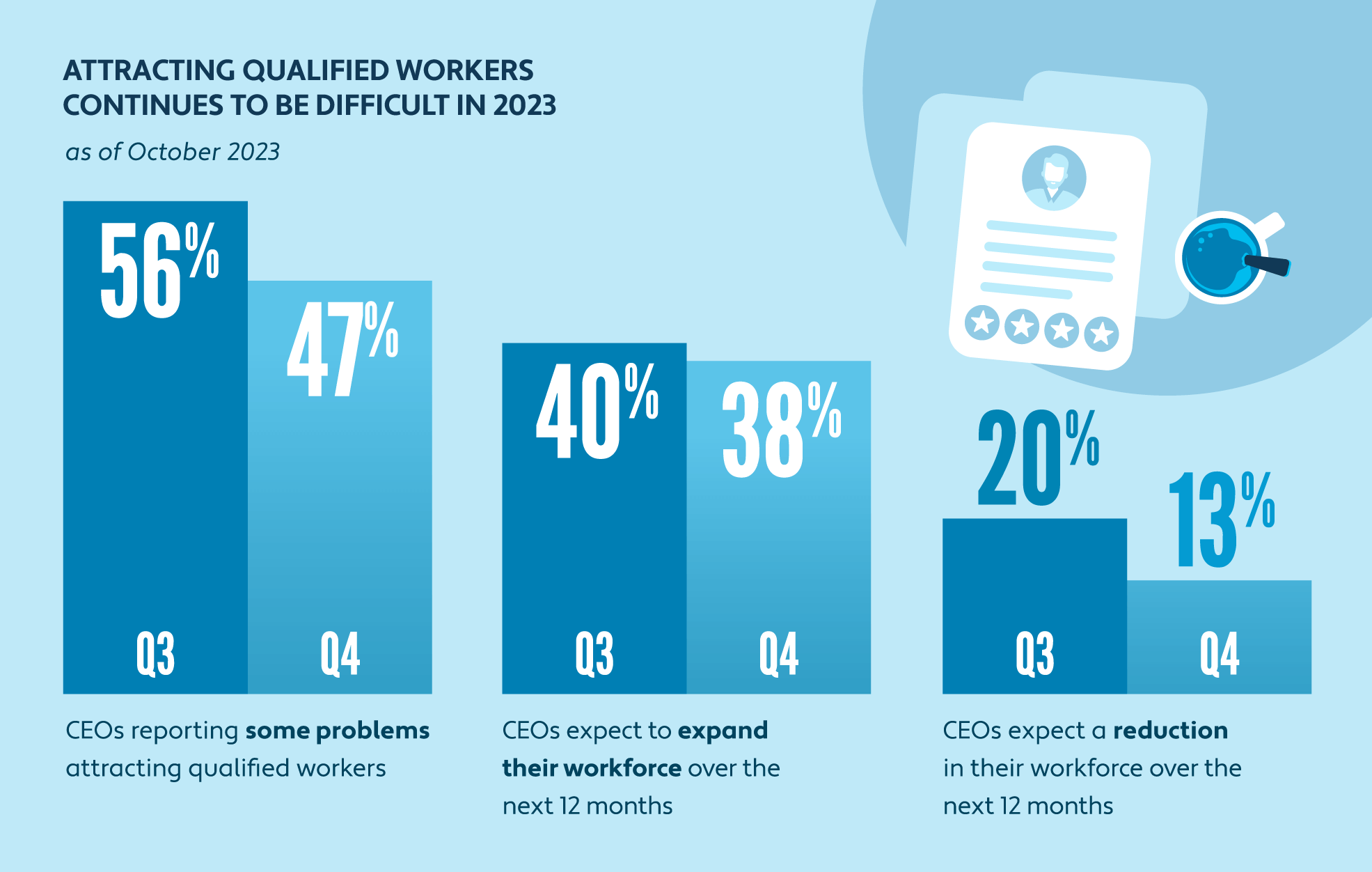

Since business must go on, recession or no, companies need people and/or technological tools to get jobs done. Unfortunately, like last year and the year before, many businesses are finding it hard to fill positions.

Employers still need talent

Attracting qualified workers continues to be difficult for many companies surveyed by The Conference Board, but the situation seems to be improving: 47% of CEOs surveyed in late September 2023 reported problems attracting qualified workers, down from 56% in Q3.

SOURCE: The Conference Board

Of CFOs surveyed in August 2023 (who could select more than one response):

81% reported a talent shortage in accounting

49% were experiencing a talent shortage in Financial Planning and Analysis (FP&A)

42% reported a talent shortage in Accounts Receivable (AR)

39% reported a talent shortage in Accounts Payable (AP)

Increasing wages can help attract and retain employees — 71% of the CEOs surveyed by The Conference Board plan to raise wages by more than 3% over the next year. But given the fierce competition for talent, some businesses are considering alternative options. Like artificial intelligence (AI).

AI’s got talent

Just over 92% of the CFOs surveyed in the U.S. and U.K. agree AI tools will help drive efficiency, productivity, and profitability for their businesses. And about 96% of the CFOs said they plan to adopt AI within their finance teams in the next 11 months.

Artificial intelligence hasn’t just caught the eye of the finance sector. The release of ChatGPT in November 2022 propelled AI into manufacturing, marketing and sales, medicine, supply chain management, and even tax compliance. There are seemingly endless possibilities for AI tools. They may even help bring byzantine government systems into the modern age.

SOURCE: McKinsey & Company

The IRS is using AI to help uncover tax evasion. The agency is relying on artificial intelligence and improved technology to help examine 75 of the nation’s largest partnerships and to identify “sophisticated schemes to avoid taxes.” AI will help IRS compliance teams “identify emerging compliance threats and improve case selection tools to avoid burdening taxpayers with needless … audits.”

Artificial intelligence can help tax officials improve compliance in other ways as well. For example, Colorado and Missouri are leveraging AI-driven Avalara Tax Research for Government to power their publicly available sales and use tax information hubs. The technology facilitates communication between state regulators and enables the states to easily keep track of ordinances, rules, taxability information, and proposed tax changes within their local jurisdictions.

Jayme Fishman, EVP and GM of Indirect Tax at Avalara, explains: “Using the best in artificial intelligence, automation, and a team of tax experts, Avalara’s solutions and database for tax compliance rates and rules help increase the accuracy and timely validation of tax data for businesses and governments alike.”

It’s a big job, because state sales tax laws are continually in flux.

The state of state sales tax

There was a good deal of state tax reform in 2023, for the third consecutive year, and that trend is looking to continue into 2024. With respect to sales tax, states are primarily focusing on a few key areas:

- Economic nexus

- Marketplace facilitator laws

- Retail delivery fees

- Sales tax holidays

- Taxability changes

SOURCE: Avalara

Trimming the fat from economic nexus laws

The United States Supreme Court decision in South Dakota v. Wayfair, Inc. celebrated its fifth anniversary on June 21, 2023, six months after the last holdout state began enforcing an economic nexus law the Wayfair ruling freed it to enact. The anniversary marked the end of a fast-paced period of rapid change that set businesses scrambling to be sales tax compliant.

States fell over themselves to adopt economic nexus in the wake of the Wayfair decision, and perhaps with good reason: Had Wayfair been successfully challenged, states could have lost the right to tax remote sales before they had the chance to benefit from the ruling.

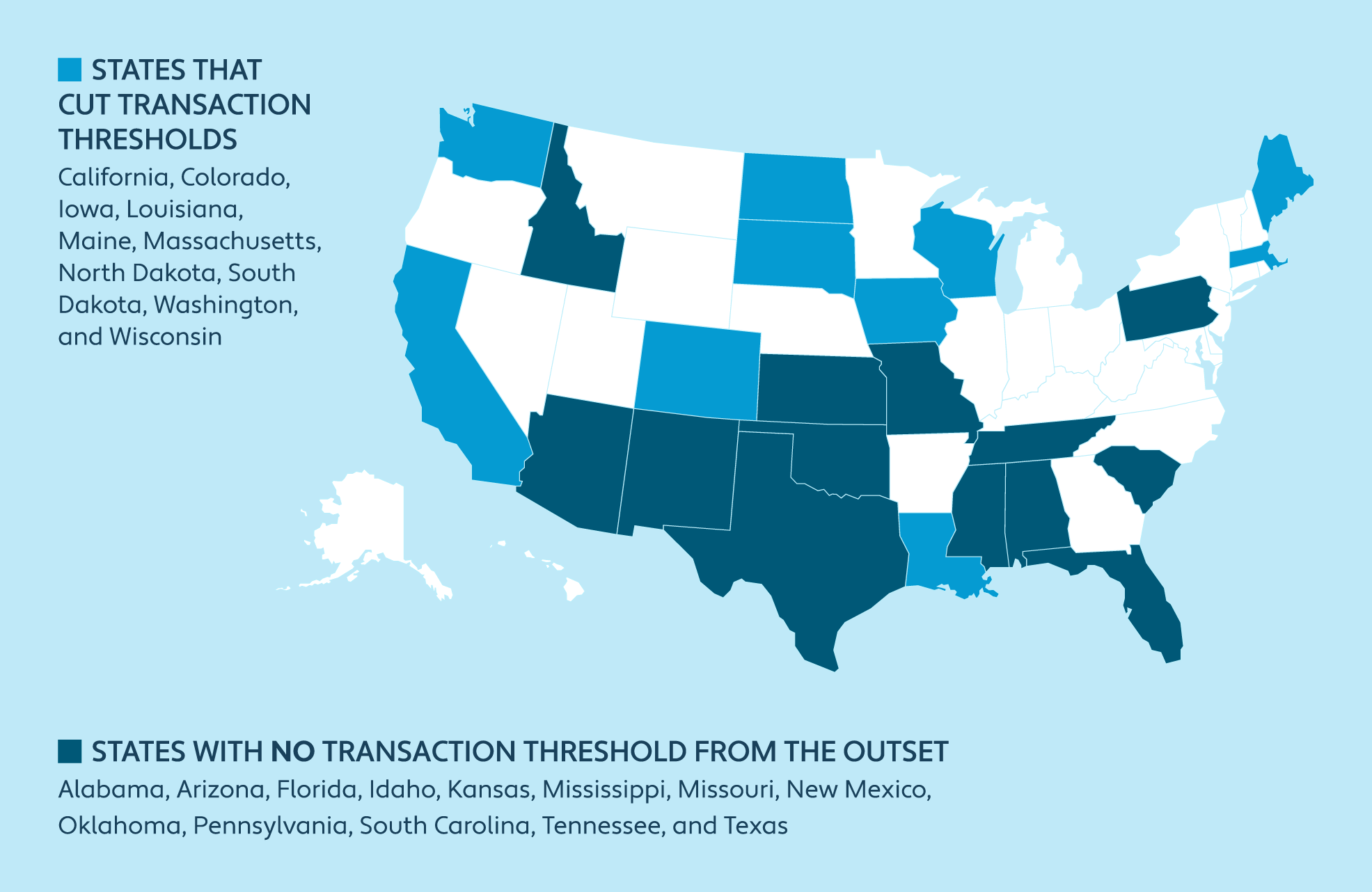

To minimize the likelihood of a legal challenge, most states followed South Dakota’s lead and set an economic nexus threshold of $100,000 in sales or 200 transactions in the state in the current or previous calendar year. But it didn’t take long for some states to reconsider those thresholds.

California was one of the first states to realize South Dakota’s threshold may not be the best fit, especially for a state with one of the world’s largest economies. As of October 1, 2023, roughly 20 states had adjusted their economic nexus thresholds in some way, and 10 states had dropped the transaction threshold — including economic nexus pioneer South Dakota.

SOURCE: Avalara

A transaction threshold is still in effect in 25 states, but that will likely change in 2024. Minnesota and Utah are gearing up to introduce legislation to this effect, having missed the opportunity during their 2023 legislative sessions. Other states will almost certainly do the same.

Moreover, the Streamlined Sales and Use Tax Governing Board (SSTGB, or simply SST), an organization dedicated to streamlining and reducing the cost of sales tax compliance for businesses, is encouraging states to get rid of their transaction thresholds. “The SST states are the majority of states that have a transaction threshold,” observes Scott Peterson, VP of Government Relations at Avalara and former Executive Director of SST. “If they get rid of it then very few states will have it.”

Peterson adds that for businesses as well as states, the amount of tax collected should be greater than the cost of compliance. “Since the Wayfair decision, states have realized there are businesses that sell a lot of very inexpensive products, producing an amount of tax that is much less than the cost of compliance.” This is the incentive behind eliminating the transaction threshold.

SST is also looking to establish a best practice for how quickly a state should require a remote business to register for sales tax after crossing an economic nexus threshold. At least eight states plus Puerto Rico and the District of Columbia currently require businesses to register as soon as they cross the economic nexus threshold.

That bears repeating: In some states, if you make a sale that puts you over the economic nexus threshold, you’re required to register and start collecting sales tax before the very next sale.

The Government Accountability Office lists registration timing as part of “a complex patchwork of requirements” in the taxation of remote sales, so it’s little wonder SST recommends states give businesses 60 days to register after they cross a state’s economic nexus threshold.

Of course, economic nexus is just one part of the remote sales tax equation. Marketplace facilitator laws are another.

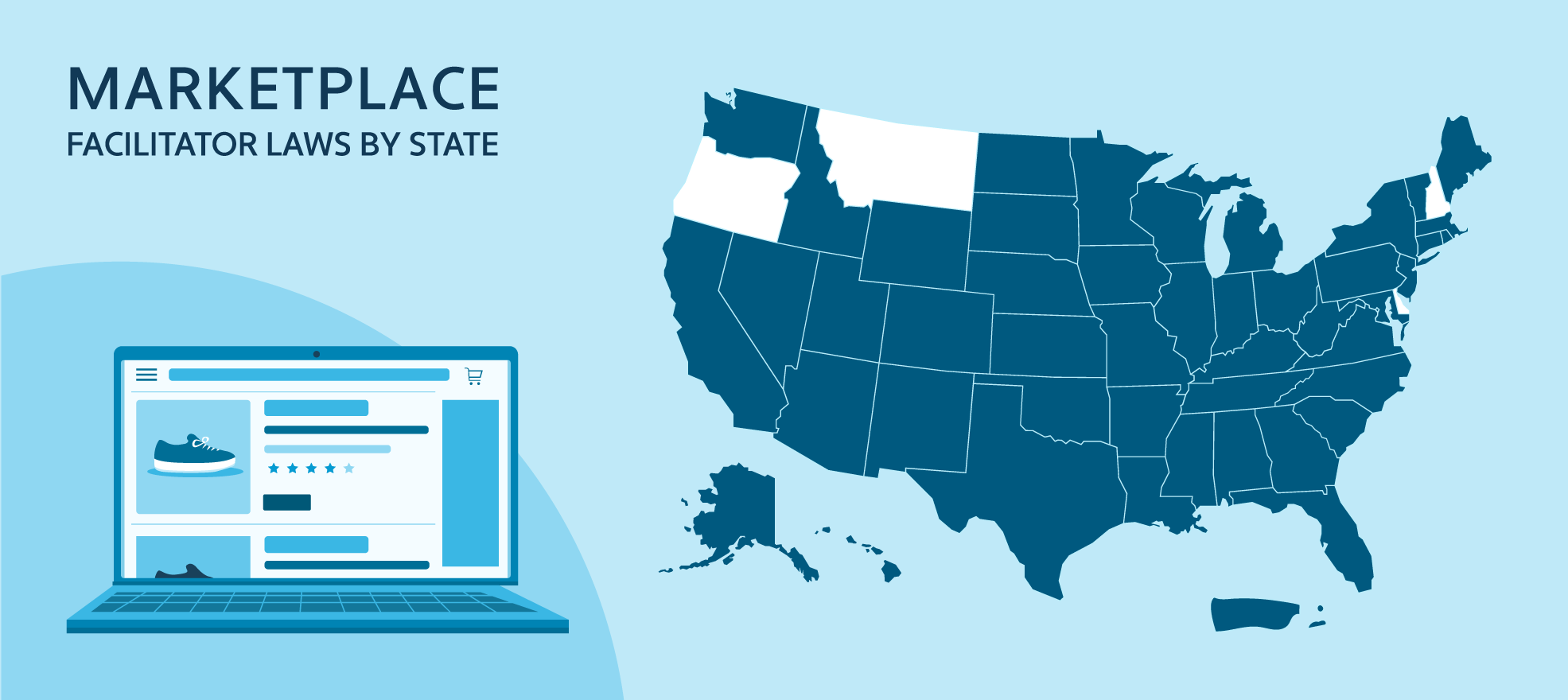

Reshaping marketplace facilitator laws

Every state’s economic nexus law provides an exception for small sellers whose sales don’t meet the state’s registration threshold. Many of those small businesses sell through marketplace platforms that help them reach a broad market. So, states created marketplace facilitator laws that enable them to capture revenue from those marketplace sales without unduly burdening the marketplace sellers. (At least this is how states view marketplace facilitator laws today; the marketplace facilitator laws origin story is much longer.)

Marketplace facilitator laws make the marketplace platform responsible for collecting and remitting the tax due on all sales made through the platform — their own (direct) sales and marketplace (third-party) sales. That’s true for all states, but beyond that, marketplace facilitator laws can vary considerably from state to state.

SOURCE: Avalara

As with economic nexus laws, many states adopted marketplace facilitator laws quickly in order to increase sales tax collections from marketplace sales. And as with economic nexus laws, many states are in the process of refining their marketplace facilitator laws. Pressing issues for states include:

- Defining what type of business is, and isn’t, a marketplace

- Establishing which taxes marketplaces facilitators are responsible for

- Understanding what marketplaces do in the metaverse

Pressing issues for marketplaces, and by extension marketplace sellers, include:

- Adhering to new consumer protection mandates (the INFORM Consumers Act)

- Complying with new 1099 reporting requirements

- Managing exempt sales (and exemption certificates)

We cover marketplace facilitator laws more in the retail, beverage alcohol, lodging, manufacturing, and software sections of this report.

Retail delivery fees: A masquerading tax

Colorado rocked retailers in 2022 by implementing a revolutionary retail delivery fee of 27 cents on all deliveries in the state that 1) are made by motor vehicle and 2) contain at least one item of taxable tangible personal property. Though inspired by the high volume of online sales, the sales-tax-masquerading-as-a-fee affects a wide range of businesses including brick-and-mortar retailers, florists, and restaurants. The fee took effect July 1, 2022, and jumped to 28 cents on July 1, 2023.

States like to watch and learn from each other, so within a year, Minnesota enacted a retail delivery fee of its own. Minnesota’s version of a retail delivery fee, which is similar but different from Colorado’s, will take effect July 1, 2024. The 50-cent fee will apply to most retail sales of tangible personal property that are delivered in Minnesota, have a retail sale price of $100 or more, and are subject to Minnesota sales tax.

In a surprise twist, Minnesota’s retail delivery fee also applies to the delivery of clothing, though clothing itself is generally exempt from sales tax in the North Star State. So that’s confusing.

Other states will likely follow Colorado and Minnesota’s lead. In fact, lawmakers introduced both New York state and New York City retail delivery fees in 2023. Though Colorado and Minnesota are the only states to enact retail delivery fees to date, there are compelling reasons for states to pursue them in the year ahead. For one, research suggests there will be 36% more delivery vehicles in inner cities by 2030.

We cover retail delivery fees more in the energy and retail sections.

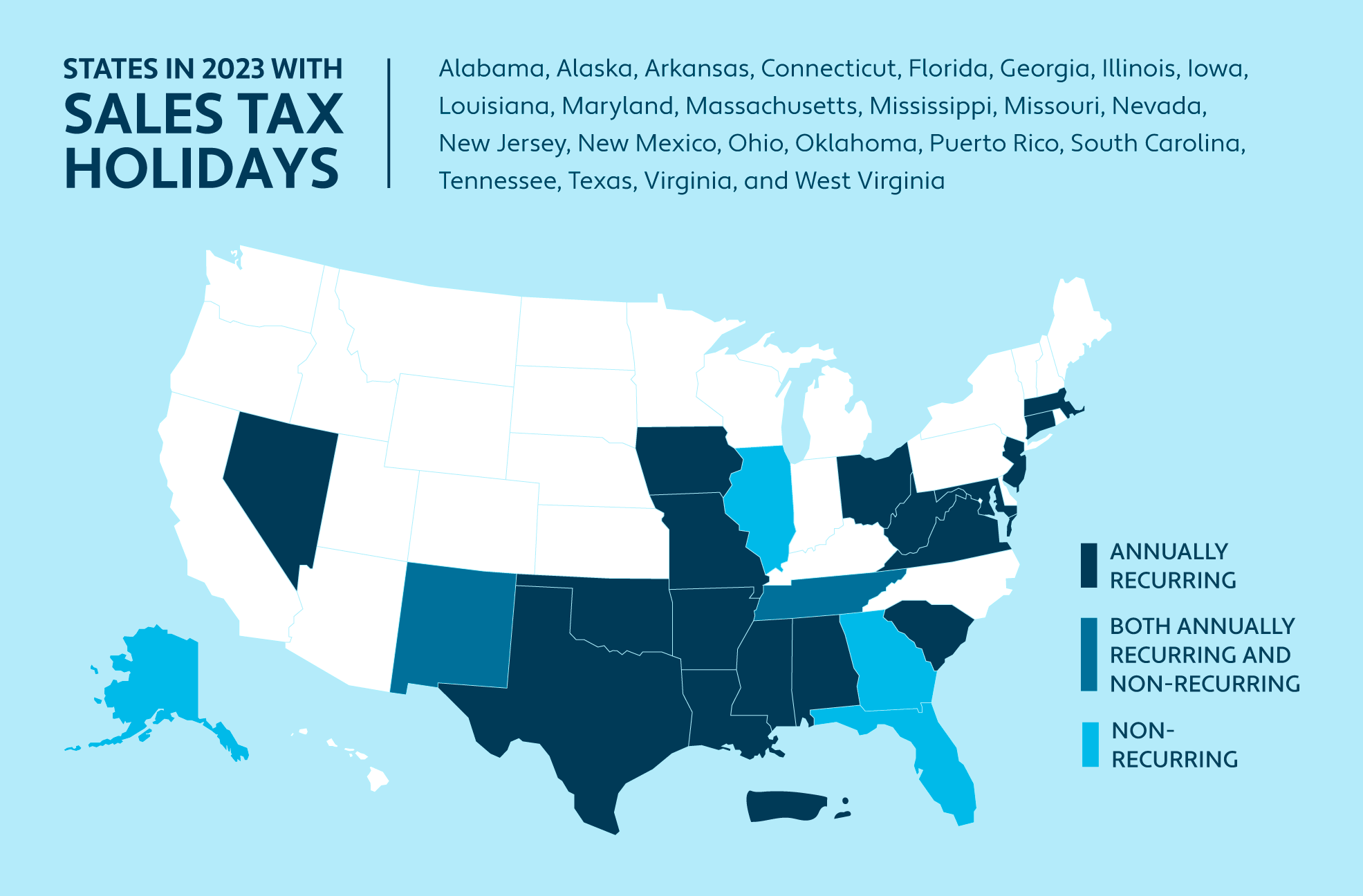

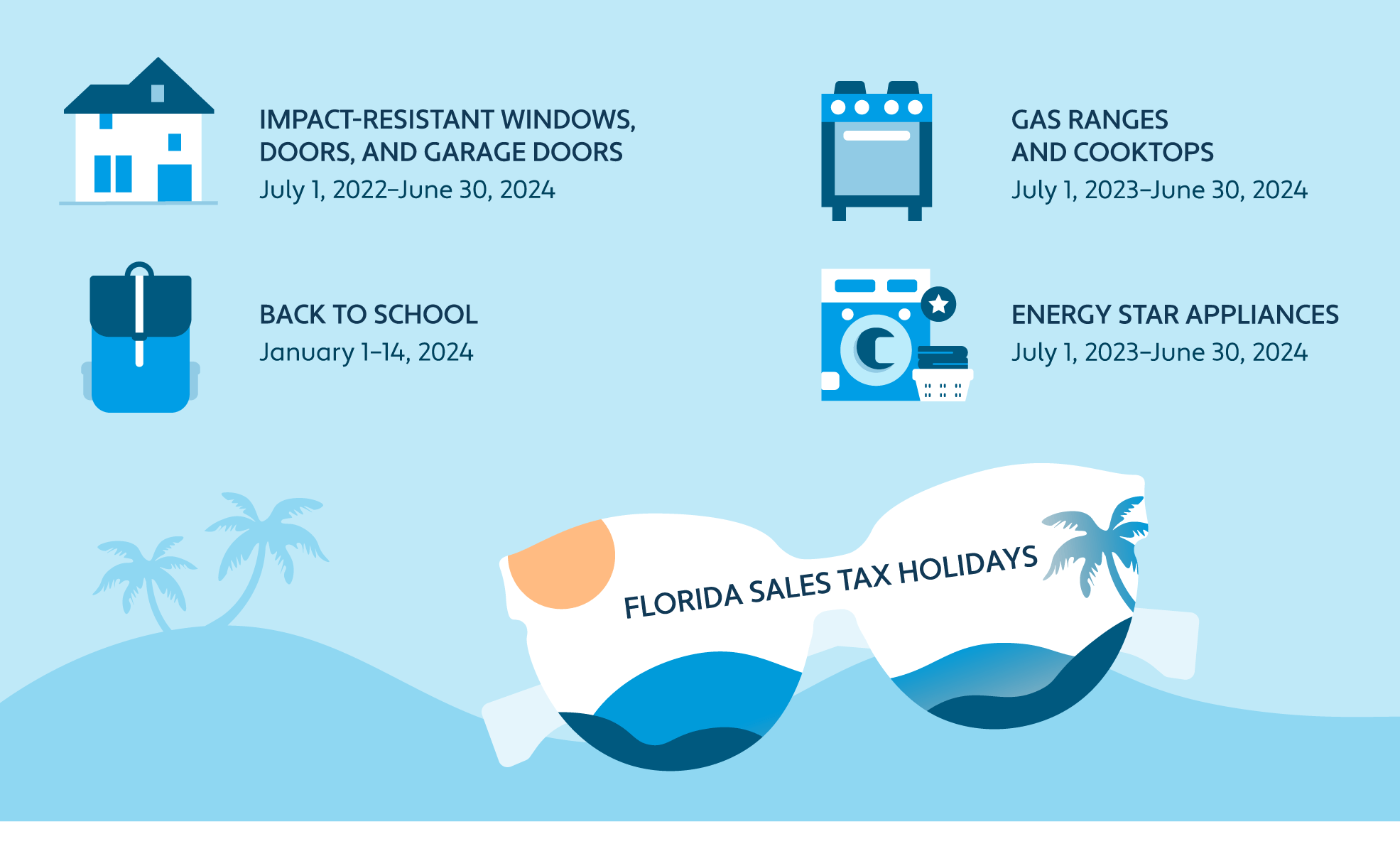

Sales tax holidays changes in 2024: Bigger. Longer. Better?

From a compliance perspective, sales tax holidays are another challenge for businesses these days. A number of states either created new sales tax holidays in 2023, or broadened or lengthened existing tax-free weekends.

Florida has stretched sales tax holidays to near breaking. A sales tax holiday is a temporary time away from sales tax. A vacation from sales tax, if you will. Vacations typically last a week or two, maybe three. Sometimes people take extended vacations. But when a vacation lasts months or even years, is it still just a holiday? Or is it something different — in this case, maybe simply a sales tax exemption?

We cover sales tax holidays in more depth in the retail section.

SOURCE: Avalara

Product taxability changes

Numerous states changed the taxability of everything from diapers and food to car seats and gun safes in 2023, and that trend will likely continue in 2024.

Most states are providing more sales tax exemptions: The few states that still tax groceries are moving toward exempting them, though at different paces; those that tax diapers and feminine hygiene products are doing the same.

For businesses that sell a variety of items into multiple jurisdictions, tracking taxability changes and implementing them into point-of-sale systems is busy work, but an essential task.

We cover taxability changes in more depth in the retail section.

State sales tax rate changes

Though statewide sales tax rates rarely change, we’ve seen a few in recent years. For example:

- The Alabama state sales and use tax rate on food went from 4% to 3% effective September 1, 2023. (Fun fact: Remote retailers that collect Alabama’s flat 8% Simplified Sellers Use Tax on all sales in the state do not benefit from the reduced rate.)

- The New Mexico state gross receipts tax (GRT) rate dropped from 5.125% to 5% on July 1, 2022, and from 5% to 4.875% on July 1, 2023; a proposal to slash the rate further in 2024 was vetoed by the governor.

The South Dakota state sales and use tax rate dropped from 4.5% to 4.2% on July 1, 2023.

A proposed seasonal sales tax rate in Maine failed to gain traction during the 2023 legislative session, and the issue isn’t likely to resurface in 2024. However, there’s at least one more state sales tax rate change planned for the near future: The South Dakota state sales and use tax rate (including for food) is set to return to 4.5% effective July 1, 2027.

While state rate changes are few and far between, changes to local sales tax rates are commonplace.

Buy local: The state of local sales tax

There are city and/or county sales and use taxes in 38 states, many of which have special district taxes as well (e.g., county ambulance districts, shopping districts, stadium districts). All told, there are more than 13,000 sales and use tax jurisdictions in the United States. Each has its own rate, and every rate is subject to change.

Local rate changes can affect out-of-state businesses as much as in-state businesses. Any business required to collect and remit sales tax in a state, whether based in the heart of the state or across the country, must collect and remit at the correct sales tax rate.

Every local rate is subject to change

Recent and upcoming local rate changes include:

Maui County, Hawaii, has a new 0.5% county surcharge in addition to the state general excise tax (GET) rate of 4%. The tax rate for transactions subject to the Maui County surcharge (CS), which is most transactions subject to the retail GET, is 4.5% starting January 1, 2024. The CS doesn’t apply to wholesale transactions, which are subject to a 0.5% GET, or to insurance commission transactions, which are taxed at a rate of 0.15%. The surcharge should help offset revenue losses caused by the August 8, 2023, wildfires.

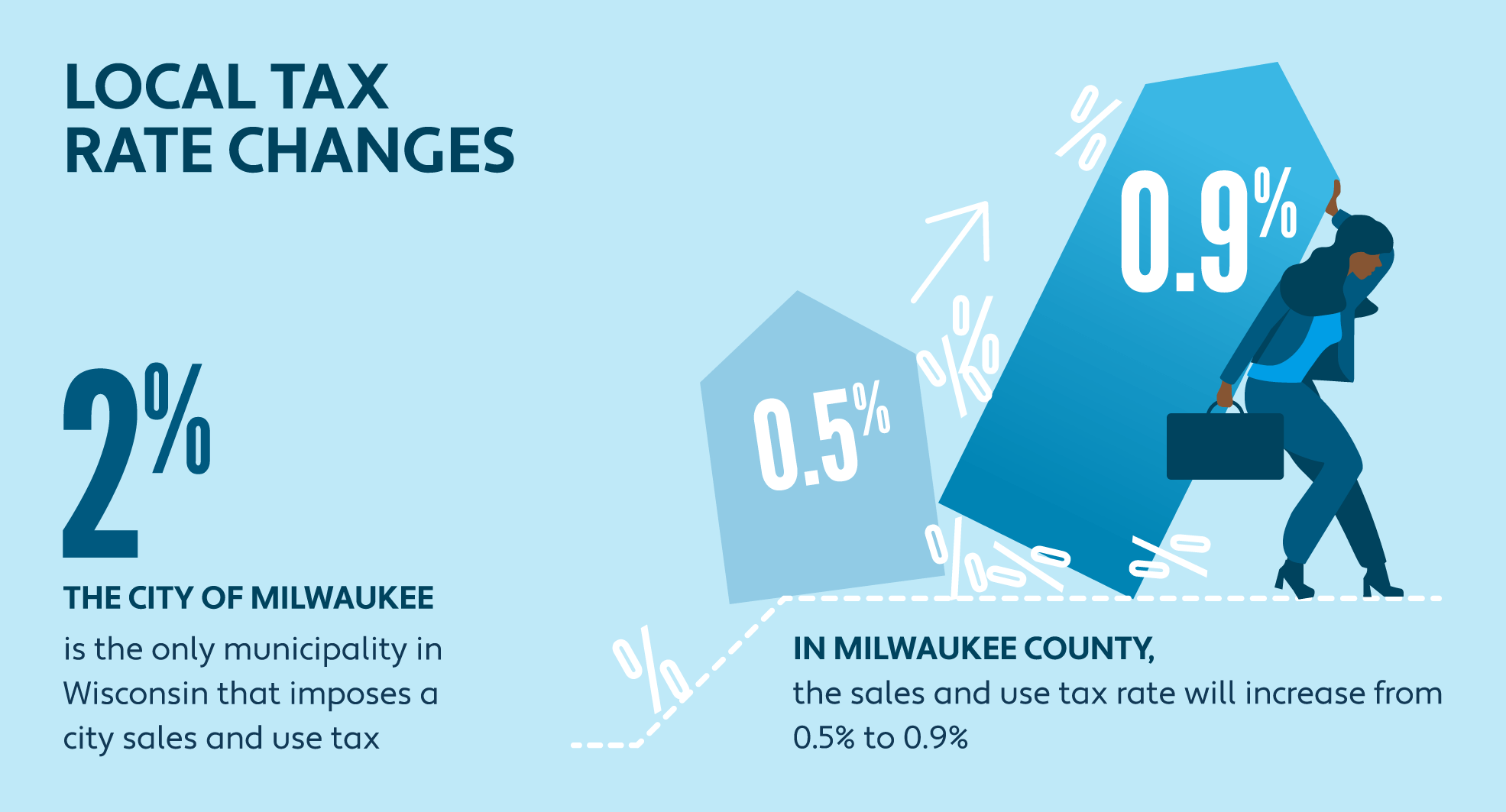

Beginning January 1, 2024, the city of Milwaukee, Wisconsin, is instituting a new 2% city sales tax to fund pensions, and the Milwaukee County sales and use tax rate increases from 0.5% to 0.9%. These tax rate changes could cause some confusion for businesses: Milwaukee is the only municipality to impose a city sales and use tax (though it affects Washington and Waukesha too), and Milwaukee County is the only county in the Badger State with a rate higher than 0.5%.

SOURCE: State of Wisconsin

The Santa Cruz, California, Metropolitan Transit District may raise the district transaction and use tax above the existing 2% combined rate limit after January 1, 2024, provided 1) the board of directors of the district adopts an ordinance approving the tax increase before January 1, 2035; 2) the total additional tax doesn’t exceed 0.5%; and 3) Santa Cruz voters approve the tax hike.

Tribal governments in New Mexico can set their own GRT rates as of July 1, 2023, “without regard to the rates in neighboring county areas.” Additionally, Taos County can now impose a local option GRT of up to 0.5% to pay for hospital capital costs and a nursing program, though the tax would need to be approved by county voters.

Three municipalities implemented a 1% local option sales tax in Vermont on July 1, 2023. With the addition of Rutland, Shelburne, and Stowe, there are 23 local option sales taxes in the Green Mountain State.

These and other local rate changes can be a headache for retailers, but the pain should be mild in states with centralized sales and use tax reporting. The migraine tends to accompany tax compliance in the country’s few home-rule states.

Simplifying home-rule tax requirements

When it comes to sales tax, “home rule” means local governments have the authority to levy and administer their own local sales tax rates and rules. This tends to make sales tax compliance extremely challenging, especially for businesses required to collect and remit sales taxes in numerous jurisdictions. Thus, all home-rule states are working to reduce the burden of compliance for businesses.

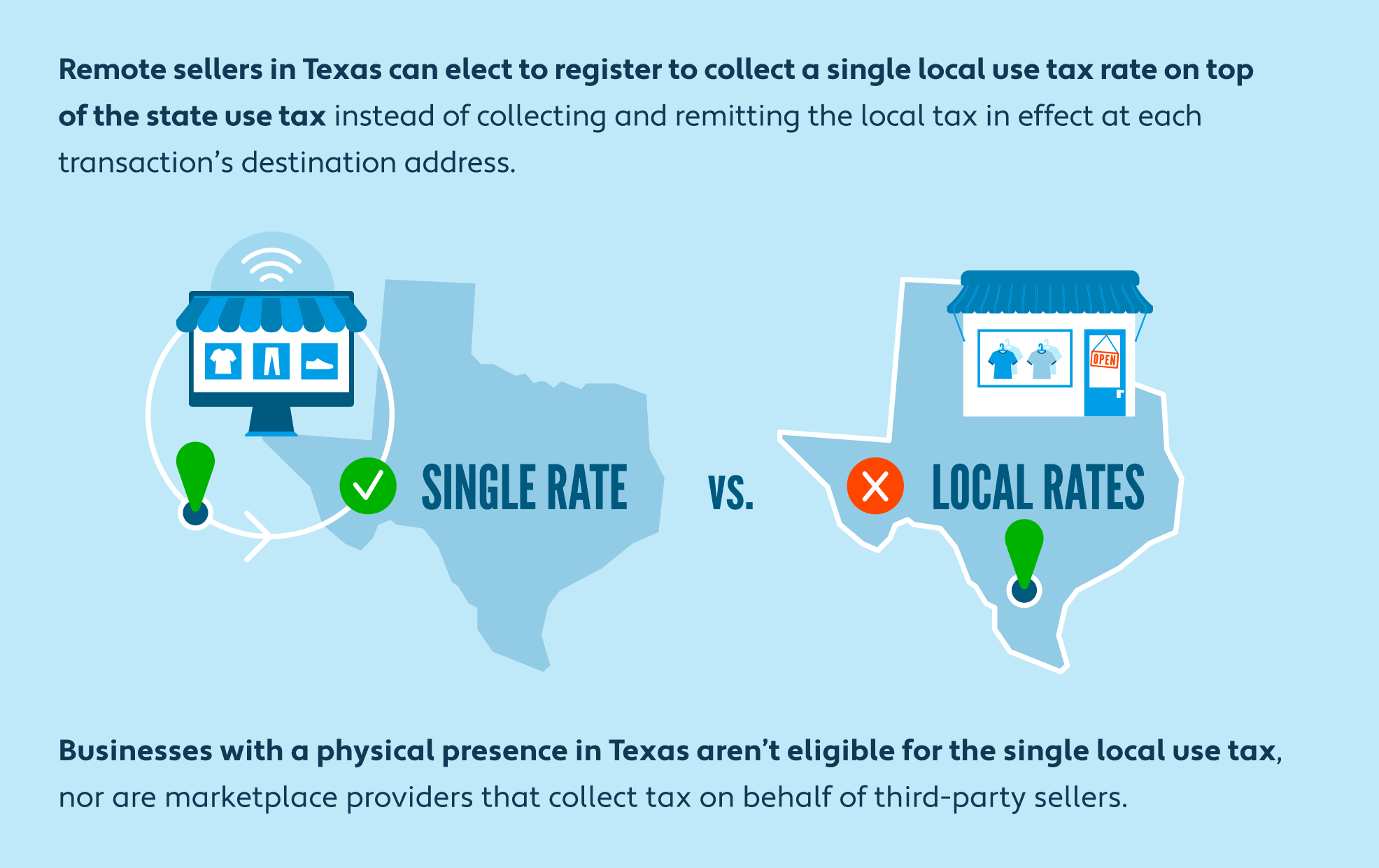

Arizona took great strides toward simplifying transaction privilege tax compliance back in 2021. The Grand Canyon State sought to further reduce compliance complexity in 2023 in several ways, including by allowing remote sellers to collect and remit a single municipal tax rate rather than the various rates in effect across the state. Unfortunately, for remote sellers, the bill did not make it into law.

Alabama, Louisiana, and Colorado have also all taken steps toward sales tax simplification, but they still have a long row to hoe.

Alabama cracks down on police jurisdictions

There are easily hundreds of local sales and use taxes in Alabama; the Alabama Department of Revenue administers some, local tax authorities administer others. This is par for the course in a home-rule state, but there’s an extra layer of complexity in Alabama because many municipalities have a police jurisdiction, and the tax rate in a police jurisdiction tends to be lower than the rate in effect in the rest of the city.

A law enacted in 2021 set a number of new requirements pertaining to annexations, deannexations, services, licenses, and taxes within a municipal police jurisdiction, in order to restrict the growth of police jurisdictions. Among other mandates, the law provides for the reporting and auditing of revenue collected within municipal police jurisdictions.

Any town or city that fails to comply with the new requirements must stop collecting taxes and fees in the police jurisdictions. Cities were given from March 2022 to March 2023 to comply with the new mandates and provide the necessary reports. Those that failed to fulfill all new obligations must cease collecting related taxes and fees.

The law states, “If a municipality fails to file a report as [required] within 12 months of the report being due, the municipality may not collect any further license revenue or any other taxes or fees in the police jurisdiction outside the corporate limits.”

Nearly 200 towns and cities with police jurisdictions have done what they need to do to comply with the law, but local licenses, taxes, and fees levied in the police jurisdictions of 127 municipalities are no longer valid and should no longer be collected as of June 1, 2023. However, licenses, taxes, and fees within a municipality’s city limits must still be collected and remitted, as must state and county licenses, taxes, and fees. Affected businesses should take note.

Fortunately, police jurisdiction rate changes shouldn’t impact remote retailers registered to collect and remit the Alabama Simplified Sellers Use Tax (SSUT). The SSUT was instituted to simplify sales tax compliance for businesses with no physical presence in the state. Instead of collecting the specific rate in effect in hundreds of different jurisdictions, SSUT-registered businesses collect a flat 8% sellers use tax on all sales made into Alabama.

SOURCE: Texas Comptroller

Louisiana’s “simple, efficient, and cost-effective” system is a work in progress

Louisiana has been working for years to simplify its complex local sales and use tax system, primarily in order to tax remote sales without placing too great a burden on out-of-state businesses. Progress is slow.

One of the first hurdles the home-rule state needs to overcome is its lack of a statewide sales and use tax collection system. Patrick Hennessey, Compliance Supervisor at Avalara, explains that there are currently three ways for customers to file and pay Louisiana sales and use tax:

- Businesses with a physical presence in the state file state-level sales tax returns and payments with the Louisiana Department of Revenue, and they file parish-level sales tax returns with the individual parishes; these can be filed on a single website, Parish E-File, which facilitates electronic filing of state and parish/city sales and use tax returns. The parishes each have their own separate return for reporting sales and use tax for all localities within the parish.

- Taxpayers that meet the remote seller threshold can file and pay all state and local sales and use tax through the Louisiana Sales and Use Tax Commission for Remote Sellers (RSC), which is the sole entity to collect sales and use tax from remote retailers as of July 1, 2020. The commission accepts only electronic returns and payments via its web-based portal and allows remote sellers to submit one return containing all necessary state and local reporting information. Remote businesses must apply to collect through the RSC.

- Taxpayers below the remote seller threshold that voluntarily collect should file and pay a direct marketer return with the Louisiana Department of Revenue (the tax rate is higher than the standard sales tax rate because local taxes aren’t required).

The RSC has reduced the complexity of sales tax compliance for remote businesses with an obligation to collect. For companies with a physical presence in the state, simplification is still a work in progress.

Home-rule local governments in Louisiana would prefer to keep levying and administering local sales taxes themselves, but the Louisiana Legislature recognizes more centralized and simplified administration of local taxes is needed.

Act 685 (2022) expands the authority of the Louisiana Sales and Use Tax Commission for Remote Sellers to collect nonremote sales and use tax on behalf of state and local sales tax collectors that enter into contracts with the commission to do so. It also requires the commission to create a single electronic sales tax return once any such contract is executed.

It will take time to implement simplification measures for nonremote sellers; as of November 1, 2023, the RSC FAQ states businesses with a physical presence in Louisiana are “subject to state and local sales tax collection and remittance requirements.”

Meanwhile, the Pelican State is moving forward with other sales tax compliance simplification measures. The Louisiana Uniform Local Sales Tax Board will begin overseeing a new uniform sales and use tax return and remittance system effective January 1, 2024. The board is tasked with designing, implementing, managing, maintaining, and supervising a single remittance system for all taxing authorities within a parish no later than January 1, 2026.

The board will also “develop a uniform reporting schedule for audit reports for all entities that serve as the single sales and use tax collector for all taxing authorities within a parish that are compensated based on the cost of collection” beginning with fiscal years ending on or after December 31, 2023.

While the transition is underway, the Louisiana Department of Revenue will continue to provide the existing local sales and use tax filing system (Parish E-File).

Under the current system, sellers need to remit to up to 64 different taxing jurisdictions in Louisiana. So, Scott Peterson thinks Louisiana local tax collectors should be congratulated for thinking outside the historical tax collection structure.

Colorado is simplifying local tax compliance for remote retailers

Like Alabama and Louisiana, Colorado is a home-rule state where local jurisdictions can independently administer local sales and use taxes. And as in Louisiana, Colorado created a centralized point of collection for remote sales tax.

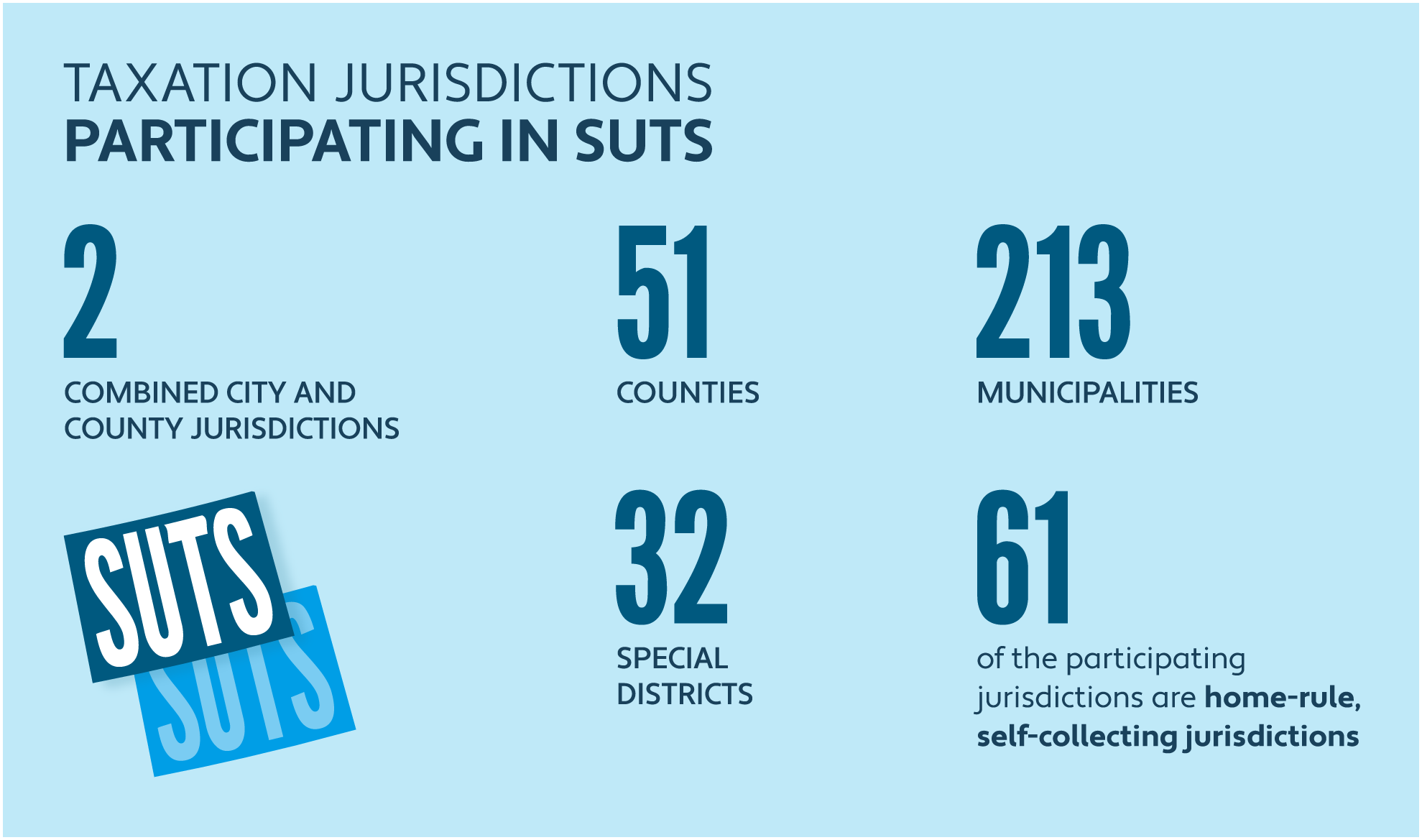

The Colorado Sales and Use Tax System, or SUTS, provides a single point for sales tax registrations, payments, and returns. The system can be used for state and state-administered local sales and use taxes as well as for self-collecting home-rule sales taxes for jurisdictions that have elected to participate in SUTS. Self-collecting home-rule municipalities must use a combined sales and use tax return in order for taxpayers to be able to report local use tax through SUTS.

SOURCE: CDOR

Colorado SUTS is using Avalara Tax Research for Government, a self-service tax management tool that leverages Geographic Information System (GIS) technology to provide sales and use tax rates and tax information. This allows businesses to identify the taxing jurisdiction related to each sale of a taxable good or service, and to look up the sales tax rate in effect at each delivery address.

Local business license requirements in Colorado also recently got a whole lot easier for some businesses. As of July 1, 2023, local governments cannot require retailers to apply for a local business license if they have “incidental physical presence” or no physical presence in the jurisdiction. This helps simplify and reduce the costs of local tax compliance in the state for affected businesses, but it doesn’t eliminate the burden of local tax compliance.

“It is great news for the taxpaying public,” says Scott Peterson, “that state and local governments are working together to understand what makes sales tax complex.”

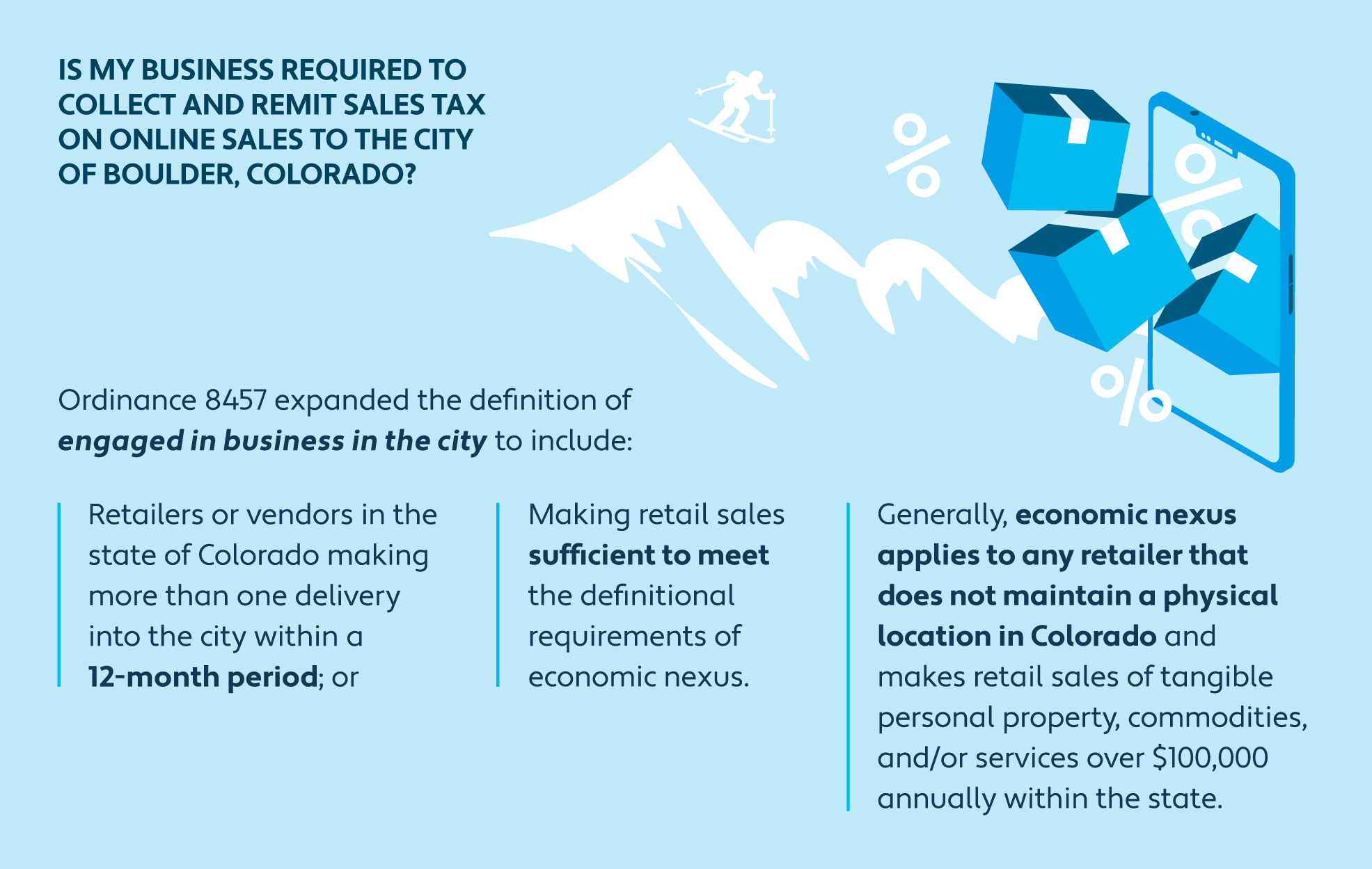

These measures are making Colorado an easier place to do business, but complications remain. For example, the City of Boulder has a local economic nexus ordinance that requires certain Colorado-based (but not Boulder-based) vendors to collect and remit online sales tax to the City of Boulder.

SOURCE: City of Boulder

State and local tax issues need digital solutions

The pandemic revealed how painfully dependent state and local governments are on in-person employees, the mail, paper, and outdated systems in general. Out of necessity, some government agencies began exploring digital or cloud-based systems after COVID-19 forced them to transition to a remote work environment — but old habits die hard.

“Some governments have been slow to harness the potential of digital technology to improve delivery of public services and strengthen public finance,” observed the International Monetary Fund (IMF) in September 2023, encouraging the public sector to accelerate and strengthen the adoption of digital solutions. “Digitalization enables governments to leverage technology to enhance revenue collection, improve efficiency of public spending, strengthen fiscal transparency and accountability, and improve education, health-service delivery, and social outcomes.”

SOURCE: IMF

A few states are now using technology to streamline sales and use tax compliance. But Scott Peterson has noticed many governments do business the same way they did 45 or 75 years ago. “Businesses will always adopt new things quicker than governments because of the difference in how decisions are made. This applies especially in technology.”

That’s starting to change, at least at the state level. At the National Association of State Chief Information Officers’ annual conference in October 2023, many state CIOs shared how their states are implementing generative AI. While some CIOs are “too busy updating their outdated enterprise IT systems to even begin thinking about adoption,” others are already using AI to streamline certain tasks.

As for the federal government, the Tax Foundation reports “the IRS is still miles behind the technology curve” despite investment in modernization.

The National Taxpayer Advocate has criticized the IRS for failing to implement scanning technology to digitally input paper returns into its computer system. Although 78% of all tax returns are filed electronically with the IRS today, during the 2022 tax filing season, the IRS had a backlog of over 21 million paper returns that had to be keystroked into the system by hand. Not only is this inefficient, it increases the risk of errors.

Peterson says states are also starting to wonder why they still have paper returns. Of course, there are always reasons: States that still accept paper returns typically do so because it’s politically challenging to mandate electronic filing, or because there’s something about the state’s computer system that would make it hard to get rid of paper returns.

What’s more, some state tax authorities are questioning why they require businesses to file sales tax returns at all when all they want is the money. Indeed Brazil, which implemented electronic invoicing in 2005, is looking to use e-invoicing data to generate pre-filled tax returns.

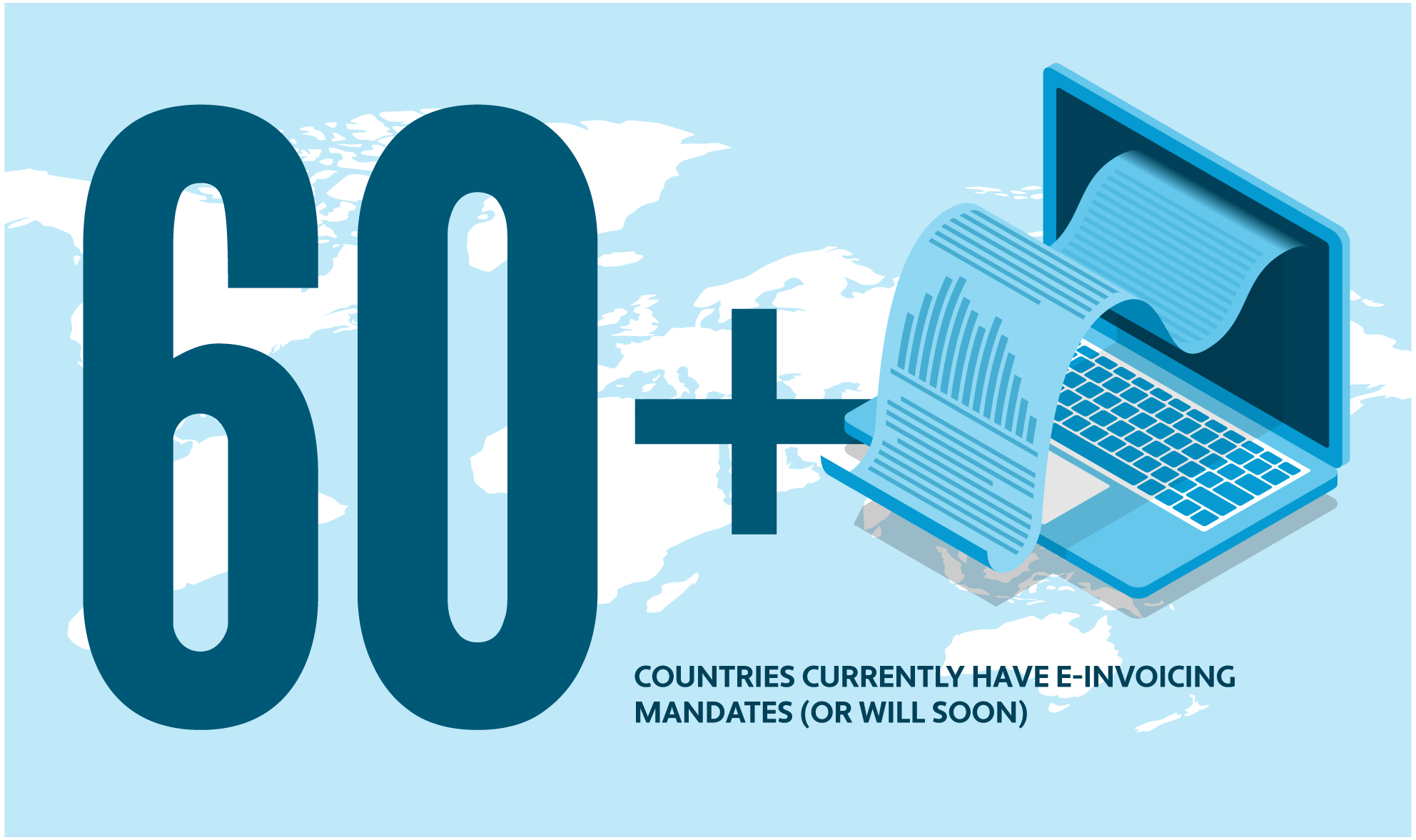

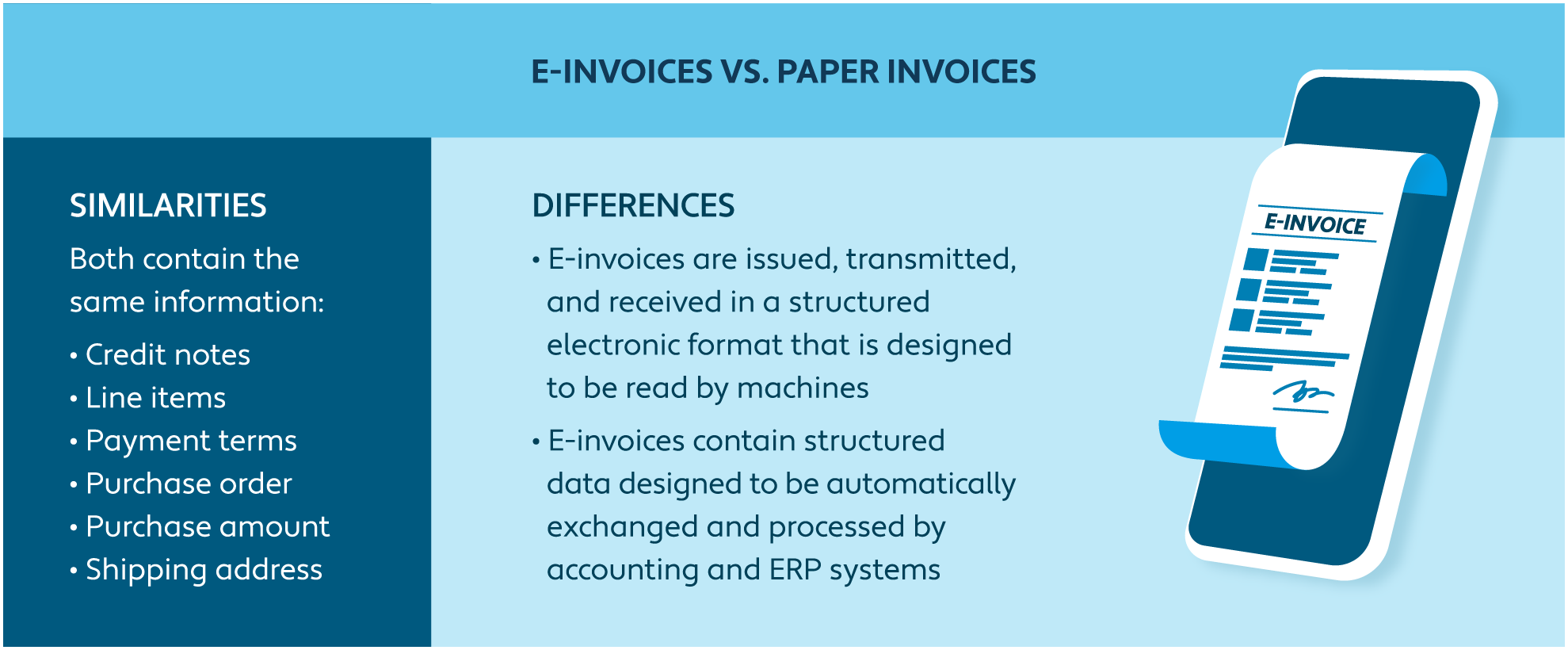

An e-invoice isn’t the same as a paper invoice that’s been uploaded into a digital format; it’s a digital file containing structured data designed to be automatically exchanged and processed by accounting and ERP systems. E-invoicing helps streamline tax reporting, increase tax collections, and reduce tax gaps (the difference between expected and actual tax collections). But while more than 60 countries currently have e-invoicing mandates (or will soon), e-invoicing remains somewhat of a foreign concept to state and local governments in the U.S.

Instead, U.S. businesses are blazing the country’s e-invoicing trail.

U.S. businesses embrace e-invoicing

Recognizing how costly and inefficient paper invoicing is for businesses, the Business Payments Coalition (BPC) launched an e-invoicing pilot project in September 2021. With support from the Federal Reserve, the BPC is creating a secure, open e-invoice delivery network for businesses to share electronic supply chain documents with one another. Avalara was a technical committee contributor for the Business Payment Coalition’s E-invoicing Exchange Market Pilot.

SOURCE: Avalara

“Businesses are interested in leveraging technology,” says Liz Armbruester, EVP of Customer and Compliance Operations at Avalara. “And Avalara can be the bridge between business and government.” Avalara intends to be accredited by the Digital Business Networks Alliance as an access point and service provider to facilitate the sending and receiving of electronic business documents over the new exchange framework.

Government tax agencies in the U.S. may be a long way from implementing any sort of e-invoicing mandates, but they’re watching what the business community is doing with interest.

“The same technology revolution that has created challenges for tax authorities also offers incredible advantages,” Armbruester observes. “Whether it’s enabling easier, simpler ways to digitally file tax returns or leveraging more complex uses of technology like clustering algorithms, ensemble modeling, or machine learning, tax authorities can make significant strides in process efficiency while enjoying the resource gains. Taking advantage of technology can help tax agencies rethink their digital workflows and data management while also enabling a better taxpayer experience and deepening the relationships with key stakeholders in the compliance workflow.”

In the meantime …

… Tax authorities are getting back to business with audits

Tax agencies throughout the U.S. are resuming audits. Using lessons learned during the pandemic, they’re increasing efficiency by consolidating travel and leaning into phone and online audits.

The Inflation Reduction Act of 2022 provides roughly $80 billion in additional IRS funding over the next 10 years, with more than $45 billion earmarked for enforcement. Some of the effects of that money could trickle down to states: If the IRS requires a taxpayer to amend a federal income tax return, for instance, the taxpayer may need to amend their state income tax return as well; so, although the enforcement money doesn’t go directly to states, states could benefit.

The IRS will also continue to collaborate with state tax administrators and software and tax professionals to increase security measures and protect against identity theft.

Businesses should bear this enhanced scrutiny in mind when grappling with compliance.

What else could affect sales tax in 2024?

Though we give it the old college try, it’s impossible for us to include everything happening with sales tax today, or to predict everything that will transpire in the year to come.

Here are some of the topics we plan to track as 2024 unfolds:

- Severe weather will cause more tax filing delays

- States will continue to grapple with the nature and taxability of NFTs

- States will examine tax policy as it pertains to ticket sales and confront tax challenges concerning collectibility, transparency, and enforcement

More states may crack down on junk fees

How Avalara can help

Avalara can help you account for tax changes and improve tax compliance for your business. Learn more about our automated solutions for calculating tax rates, preparing returns, and managing documents.

Discover more tax changes in our industry sections.